Panel at the second international summit on food production in Dakar, 10 February 2023, from left to right: Allan Kasujja, BBC (moderator); Admassu Tadesse, Trade and Development Bank; Danladi Verheijen, Verod Capital; M. Malick Ndiaye, Banque Agricole; Dr. Olagunju Ashimolowo, ECOWAS Bank for Investment and Development; M. Wagner Albuquerque de Almeida, International Finance Corporation. Source: African Development Bank Group

"Agriculture must become Africa's new oil," said Akinwumi Adesina, President of the African Development Bank (AfDB), at the inauguration of the "Feed Africa: Food Sovereignty and Resilience" (Dakar 2) summit, held in late January 2023 in Senegal. He spoke to 34 African heads of state and 70 ministers, representatives of the European Commission, the United States and several European countries, as well as multilateral institutions such as the International Fund for Agricultural Development (IFAD).[1]

While one of the main objectives of the Bank at the summit was to attract private financing for its projects, the intervention of the director of the Nigerian private equity fund Verod Capital explains the challenge: "I know that we talk about the future of Africa as being that of smallholder farmers, but (...), it is really difficult to experience governance at this level. Smallholder farmers are not the most efficient enterprises. Their bargaining power is limited, they have less money to invest in the infrastructure needed for more efficient agriculture and to get their products to market (…). So, we need bigger businesses where we can deploy capital. I think it will attract more private capital. »[2] Verod is one of the 70 private equity funds in which the AfDB is a shareholder.[3]

In financial terms, the Bank has a certain weight in the continent. It currently has USD 240 billion to invest and a portfolio of USD 56.6 billion already invested.[4] The main sectors covered by this portfolio are: transport (27%), electricity (20%), finance (18%) and agriculture (13%).[5]

Often these investments lead to conflicts with affected local communities. According to the Environmental Justice Atlas, the Bank is involved in at least 14 ongoing social and environmental conflicts.[6] It is in this context that social movements and women's groups are preparing an African civil society campaign against the AfDB.[7]

So how does the Bank work? Which actors benefit the most? What agricultural model is it promoting? And what role does it play in relation to the struggles for food sovereignty in Africa?

Dakar 2 and the Era of Pacts

Among the “successes” of Dakar 2 claimed by the AfDB is the agreement to implement the “Food and Agricultural Supply Pacts” for 40 countries for the next 5 years.[8] The African Union has declared its strong support for this initiative.[9]

A first reading of the pacts surprises by the lack of care taken in their drafting. For example, the pacts of Burundi and Cape Verde are incomplete, and that of Togo does not make it possible to know whether it concerns this country, Niger or Madagascar. In others, like that of Cameroon, certain parts of the text are copied several times. Despite the supposed importance of these initiatives in attracting funding from the private sector and development banks and agencies, the total cost of the projects is unclear. Our conservative estimate of the total cost is around USD 65 billion.[10]

Far from promoting agro-biodiversity, which is Africa's wealth, the pacts aim to promote mainly corn, wheat, rice, soybeans and palm oil. The aim is to increase their yields through the industrialisation of "value chains", which will extend to livestock, dairy and fisheries. To do this, the pacts will promote mechanisation, certified seeds, chemical fertilisers and pesticides, often via tax exemption on imports and other types of subsidies.

Throughout the summit it was repeated that 65% of the world's uncultivated arable land is in Africa.[11] This is why the expansion of cultivated area is strongly on the agenda in the pacts and covers tens, hundreds of thousands or even millions of hectares, depending on the country. For example, under the Tanzania pact, only 23% of the land available for agriculture would be cultivated. The document proposes prioritising the production of wheat, avocado, market garden produce and sunflower. For this, it refers to the need to expand the agricultural area by more than two million hectares by 2025, in particular through a "transfer" of land currently owned by the village councils. The government is reportedly already identifying and acquiring land for industrial agriculture, installing irrigation infrastructure, an agreement with the "Building Better Tomorrow" initiative.[12]

The provision of open trade policies aimed at attracting investment, especially from the private sector, is also mentioned in the pacts, often in the form of very problematic public-private partnerships.[13] Among other policies aimed at attracting investment, the Kenya pact refers to the absence of restrictions on the repatriation of earnings and capital. It is also worrying that the pacts are based on failed agro-industrial programs. This is the case, for example, of that of Gabon, which specifies that the implementation will be based "on the institutional mechanism already existing and set up by the support project for the GRAINE program". This program was entrusted to a public-private partnership between the Gabonese government and the multinational Olam in 2015. It has been denounced by the affected communities for having led to the grabbing of thousands of hectares by oil palm plantations.[14]

How will the pacts be funded? According to the AfDB, investment pledges have steadily increased since Dakar 2. In May 2023 they were expected to reach USD 72 billion.[15] The main institutions to contribute would be the AfDB (USD 10 billion), the Islamic Development Bank (USD 7 billion), Germany (USD 14.34 billion), the United States (USD 5 billion), IFAD (USD 3 billion) and the Netherlands (USD 450 million). Other donors identified would be the European Union, the European Investment Bank, the West African Development Bank, the Arab Bank for Economic Development in Africa, the French Development Agency, Ireland, Switzerland and the United Kingdom.[16] However, in some cases, such as that of Germany, it is not at all clear whether these funding pledges are really new and intended for compacts, or rather refer to financial support provided to projects already in place. Another important question remains unanswered: what would be the impact of financing the pacts on the external public debt of African countries, whose interest payments in 2022 amounted to USD 44 billion?[17]

Beyond the announcements, everything indicates that the pacts will only continue the implementation of the old recipe of the Green Revolution and the unwavering policy of the AfDB to promote agribusiness.

What is AfDB?

To better understand the AfDB today, it is worth recalling its origin. It was created in 1964, in the context of the access to independence of several African countries. According to some, European countries, and former colonial powers such as France and the United Kingdom in particular, were wary of an all-African financial entity, fearing an erosion of their power. On the other hand, the United States and the former Soviet Union, in the midst of the Cold War, saw the interest in increasing their presence on the continent. The World Bank was not unfavorable either, and indeed it served as a model for establishing the structure of the new bank.[18]

The debt crisis of the early 1980s marked a double turning point. If until then the peculiarity of the AfDB was that only African States could become members, the doors were opened to countries outside Africa, citing the lack of economic resources as an argument.[19] The second change lies in alignment with the structural adjustment programs launched by the World Bank and the International Monetary Fund. In this way, the AfDB contributed to the pressure exerted on African countries by the Bretton Woods institutions and rich countries to open up their economies to the market economy, with devastating effects.[20] Since then, the Bank has embraced the neoliberal agenda. For example, it is currently one of the actors which most promotes the African Continental Free Trade Area (AfCFTA)[21]

For the AfDB, strengthening the private sector is a priority. In 2020, direct investments in companies amounted to USD 636 million, and those in investment funds to 1.3 billion.[22] This orientation clearly characterizes its agenda in the field of agriculture.

Agribusiness, at any price?

As early as 1997 the agricultural sector was classified as strategic by the AfDB.[23] To date, 1,161 agriculture-related projects have been finalised or approved, for the equivalent of USD 18.4 billion.[24] In 2022 this sector accounted for 23% (USD 1.9 billion) of its loans, grants and equity investments as well as approved guarantees. The Feed Africa program took the lion's share with 1.7 billion.[25] These funds would have been used in particular to build or rehabilitate 1,682 km of roads and provide 2,605 tons of agricultural inputs (fertilisers, seeds, pesticides).[26] Between 2016 and 2025 "Feed Africa" planned an investment of 24 billion dollars to transform African agriculture.[27]

In what direction is this "transformation" heading? According to the Bank, Africa's agrifood market has the potential to reach a value of USD 1 trillion by 2030. But for that to happen, "barriers to agricultural development" would have to be removed. These would lie in the fact that a majority of farms are small, and in the lack of infrastructure and financing. To address this, the AfDB proposes leveraging private sector investment, which would “increase local productivity, develop supporting infrastructure, climate-smart agricultural systems, and introduce improvements along food value chains.”[28]

The main objective is "agro-industrialisation". What the AfDB means by this is a shift from diversified agricultural activity focused on subsistence to commercial agriculture with better access to markets and agribusiness.[29] For this, it has divided the continent into areas in which certain sectors must be prioritised: wheat in North Africa; sorghum, millet, cowpea and livestock in the Sahel; rice in West Africa; corn, soy, livestock and dairy in the Guinea Savannah; cocoa, coffee, cashew, palm oil, horticulture and fisheries across the continent.[30]

In 2017, the AfDB launched the Technologies for African Agricultural Transformation (TAAT) initiative to reduce African food imports. Since its inception, TAAT has reportedly raised over USD 800 million.[31] One of its goals is to move towards regional business investments for seed companies.[32] Multinationals such as BASF, Bayer/Monsanto, Corteva, Seed Co and Syngenta have been associated with this initiative. According to a complaint by whistleblowers that was ultimately deemed baseless by the AfDB Ethics Committee, President Adesina was involved in a USD 5 million contract under the TAAT initiative in 2017, which allegedly benefited Syngenta by violating internal funding rules. The multinational would even have delivered the insecticides for the seed treatment covered by the contract before its official selection.[33] Since then, TAAT has continued the collaboration with Syngenta.[34]

Other partnerships have also been forged.[35] In a meeting with Yara, the world's largest fertiliser company, and the Norwegian government, Adesina said, “The TAAT program, supported by the Bill and Melinda Gates Foundation, the Alliance for a Green Revolution in Africa and others, is delivering impressive results on the ground, on farms across Africa, increasing agricultural productivity and showing that Africa can truly feed itself. »[36]

The TAAT program also revolves around "climate-smart agriculture". This includes, for example, water-saving maize or heat-tolerant wheat, distributed in partnership with the seed industry. These initiatives have been denounced by civil society for the dangers they represent for food sovereignty and the perverse effect on the climate crisis they can cause.[37]

The harmful impacts on soils and the environment caused by chemical fertilisers, which do not, however, ensure a greater yield in the long term, are recognised at the international level. Equally evident are the growing profits that a handful of multinationals are making in this particular sector.[38] However, fertilisers represent one of the industries most supported by the AfDB. In 2014, it granted a loan to Dangote - Africa's richest businessman - for the amount of USD 300 million intended for the construction of a crude oil refinery and a fertiliser manufacturing plant.[39] A specific programme is dedicated to increasing the use of these products by farmers: the African Fertiliser Financing Mechanism (AFFM), created in 2006. For the current 2022-2028 period, the expected result is the distribution of 2 million tons of fertiliser and other inputs to 16 million smallholder farmers, so that they apply at least 50 kg per hectare.[40] The priority crops for this program are maize, rice, cassava, soybeans, wheat, sorghum, millet, cowpea, cocoa, coffee, cotton, horticulture and oil palm.[41]

Multinationals reap juicy profits from this program. For example, in 2019, MAFE approved commercial credit guarantee projects for fertiliser financing in Nigeria and Tanzania for USD 5.4 million.[42] In Tanzania, the credit enabled three companies, including Yara and Seed Co, to sell fertilisers worth USD 26.3 million to 570,000 farmers through agro-dealers, while in Nigeria, fertilisers worth USD 11.2 million were marketed.[43] The following year, the mechanism approved a partial credit line guarantee of USD 4 million to a subsidiary of the Moroccan multinational OCP, to provide fertiliser for three years to 430,000 small producers in Côte d'Ivoire (rice production) and Ghana (maize and rice production).[44] In 2023, the MAFE planned commercial credit guarantee schemes for a total of USD 9.7 million in Tanzania, Uganda, Mozambique and Kenya.[45]

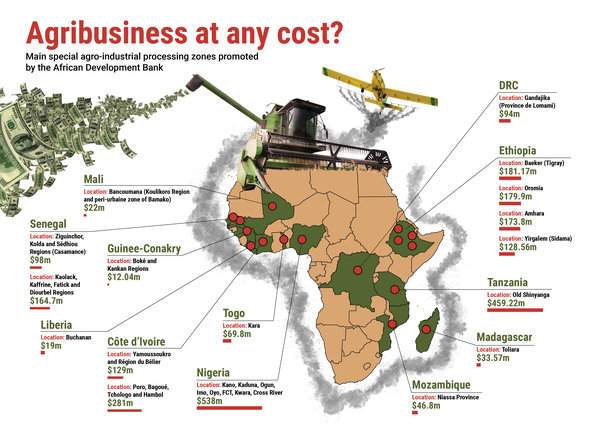

Special agro-industrial processing zones

At the Dakar 2 Summit, Special Agro-Industrial Processing Zones (SAPZs) were presented as an essential tool for having the infrastructure and logistics necessary for the creation of markets and “competitive food and agricultural value chains”.[46] Following on from the “agropoles” of previous years, these zones are also presented as fundamental in the development strategy of the AfCFTA of the African Union.

Since 2017, the Bank has reportedly committed more than USD 840 million for the development of SAPZs. Already, areas are in the preparation stage, have been approved or are in the construction phase in 14 countries, while 3 others would like to host them.[47], [48] [See table below]

In cases where the legal framework needs to be "adapted" to these projects, the AfDB does not hesitate to use loans as leverage. For example, the TANY Collective denounced the fact that in 2019 a disbursement of the AfDB's Economic Competitiveness Application Program was conditional on the adoption of a decree creating agropoles in Madagascar.[49]

Special Economic Zones: A Red Carpet for the Private Sector

Globally, there are currently believed to be as many as 7,000 Special Economic Zones (SEZs) in general, across all industries.[50] The first were established in Asia in the 1970s, followed by Latin America the following decade, and then Africa in the 1990s. In 2019, the United Nations estimated that there were 237 in 37 African countries with only half fully operational. In total, 43% of African SEZs are managed by the state, 41% by the private sector (mainly in Kenya, Ethiopia and Tanzania) and the rest are under the responsibility of public-private partnerships.[51]

Depending on the country, these zones can take different forms: free trade zones, export processing zones, free ports, industrial zones or agro-industrial parks ("agropoles"). What they have in common is that the States bear the costs of the associated infrastructure and set up special regimes in order to attract private investment. Among these measures are: customs duty exemptions for imports and exports, tax exemptions, exemptions in labor laws, repatriation of profits and guarantees for loans. In addition, companies can benefit from reduced prices for energy and water.

The land issue is particularly problematic in these areas. They are in most cases established on community land expropriated by the State and offered to investors. The area occupied by the facilities is not necessarily very large, but their location generates problems in terms of access to land, price increases, speculation and evictions.[52] The Bagré agropole in Burkina Faso is a good example. Started in 2016, this project was marked by a lack of consultation with local populations, endangering their food security, environmental risks and land disputes.[53] Indeed, foreign investors were granted 60% of the developed areas.[54] Nearly 9,000 farmers were affected, 5,000 of whom are still waiting for their land titles.[55] Although the promise was to create 30,000 jobs, young people have left the area to look for work elsewhere.[56]

The Special Agro-Industrial Processing Zones currently proposed by the AfDB differ little from other SEZ projects, other than focusing on the agricultural sector (including livestock, fisheries and forestry).[57] They include the production, processing, storage, transport and marketing of agricultural products, with a focus on increasing productivity and reducing costs. But the projects often require other road construction or rehabilitation initiatives, as well as energy and transport infrastructure, all of which have impacts on the local population.[58] For example, the SAPZ Agropole-Centre in Senegal is linked to external infrastructure projects, such as the Trans-Gambia Bridge, the future Ndayana deep-water port and a road, rail and port integration project. According to the project assessment, the main environmental and social risks are air, water and soil pollution. Land conflicts in Fatick and Kaolack are also expected due to the displacement of communities to build platforms on 140 hectares.[59]

As with all Special Economic Zones, SAPZs aim in particular to attract private sector investment. Among the various actors identified in this type of project are the major investors, who own and manage production and processing units, and subcontract small and medium-sized enterprises. Large-scale irrigation infrastructure, outreach and training services are included in these initiatives.[60] As for the peasantry, they are supposed to supply their products to aggregation platforms via contracting. The latter is an increasingly common strategy used by companies to avoid buying land. In most cases, farmers must devote their entire plot to the requested crop. The granting of credit to access agro-industrial inputs is presented as an element of the contract that benefits the peasantry. However, it entails a risk of massive indebtedness which can result in the loss of agricultural land.[61]

Click on image to zoom. Design: Evan Clayburg

Click on image to zoom. Design: Evan Clayburg

It is equally worrying to note the extent of the areas that the SAPZs claim to integrate. For example, the one launched in March 2023 in Mali (Koulikoro region and peri-urban area of Bamako), at an estimated cost of USD 22 million, plans to develop 2,921 hectares for agricultural activities, but in all, the objective is to cover 60,000 hectares of agricultural land. And this would only be the pilot phase for the construction of 12 agropoles throughout the country, at a total cost of USD 900 million.[62]

Everything suggests that these projects represent a significant territorial reorganisation, which allows agro-industry to have access not only to raw materials (fertile land with good irrigation potential), but also to cheap labour.[63] Indeed, the idea is to set up agro-industrial parks or poles that connect, as far as possible, the rural sector with peri-urban areas of secondary cities, where poverty and the number of unemployed people are high. Paradoxically, the Green Revolution played a leading role in the expulsion of peasant communities and their exodus to African cities.[64]

The AfDB must stop being the new Trojan horse of agribusiness in Africa

The territorial reconfiguration of the continent by and for the interests of big business, of which the AfDB is an accomplice, is a stark reminder of the division of Africa by the colonial powers. This time, however, the reconfiguration is being carried out by African public authorities.

The examples discussed here paint a worrying picture of the Bank's direction. All the more so as the great absentee from its programmes is peasant agriculture. Small-scale farmers, fishermen and pastoralists produce and supply nearly 80% of the food consumed on the continent. This is possible thanks to good management of seeds, water and soil, technologies adapted to processing and short supply chains. In many of these activities, women play a leading role. Every day, this model demonstrates not only its essential role in feeding and nourishing families, but also its remarkable climate resilience.[65]

But instead of being protected, peasant agriculture and the local food systems that depend on it are being systematically undermined by the AfDB's agribusiness policies and projects.

The deep, structural problems behind the Bank’s policy orientation will not be resolved by greater civil society participation in Bank meetings. The Bank must make a radical change in its approach and management of public funds, in order to respond responsibly and effectively to the food and climate crises in Africa.[66]

Main special agro-industrial processing zones promoted by the African Development Bank (AfDB) | ||||

Country | Project name | Location | Total cost (millions of dollars) | Sources |

Côte d'Ivoire | 2 PAI-Bélier | Yamoussoukro and Région du Bélier | 129 | |

Côte d'Ivoire | 2 PAI - Nord | 4 regions: Poro, Bagoué, Tchologo and Hambol | 281 | |

Mali | Development Program for the Special Agro-Industrial Processing Zone of Koulikoro and Peri-urban Bamako (PDZSTA-KB) | Bancoumana (Koulikoro Region and Peri-urban zone of Bamako) | 22 | |

Senegal | PZTA-Sud or Agropole Sud | Ziguinchor, Kolda and Sédhiou Regions (Casamance) | 98 | AfDB, « Sénégal - Projet Zone de Transformation Agro-industrielle du Sud (PZTA-Sud ou Agropole Sud) », s/d AfDB, « Projet Zone de Transformation Agro-industrielle du Sud (PZTA-Sud ou Agropole Sud). Rapport d’évaluation de projet », December 2019 BRL Ingénierie, « Évaluation environnementale et sociale stratégique », June 2023 Financial support from the German government is also mentioned without detail. (UNIDO, “Theme 2: creation of industrial zones/special economic zones. PCP intervention in Senegal”, February 2021). The United Nations Industrial Development Organization (UNIDO) carried out the first studies for the planning of the agropole ("Adéane: relive the launch of the Agropole Sud by Minister Moustapha Diop", ZigActu, December 21, 2021) |

Senegal | PZTA-Centre | Kaolack, Kaffrine, Fatick and Diourbel Regions | 164,7 | |

Guinea-Conakry | Program for the Development of Special Agro-Industrial Processing Zones (PDZSTA-BK) | Boké and Kankan Regions | 12,04 | |

Ethiopia | Integrated agro-industrial park of Baeker | Baeker (Tigray) | 181,17 | |

Ethiopia | Integrated agro-industrial park of Bulbula | Oromia | 179,9 | |

Ethiopia | Integrated agro-industrial park of Bure | Amhara | 173,8 | |

Ethiopia | Integrated agro-industrial park of Yirgalem | Yirgalem (Sidama) | 128,56 | |

Togo | Agri-food processing project (PTA-TOGO) | Kara | 69,8 | |

Madagascar | Agro-industrial processing zone in the South West Region of Madagascar (PTASO) | Toliara | 33,57 | |

Liberia | Special agro-industrial processing zone | Buchanan | 19 | |

Nigeria | Special Agro-Industrial Processing Zones Program, Phase I (SAPZ I) | Kano, Kaduna, Ogun, Imo, Oyo, FCT, Kwara, Cross River | 538 | |

DRC | Support program for the agro-industrial development of Ngandajika (PRODAN) | Gandajika (Lomami Province) | 94 | |

Tanzania | Special agro-industrial processing zone (Lake Zone) | Old Shinyanga | 459,22 | |

Mozambique | Integrated Development Corridor Agro-Industrial Processing Special Zone of Pemba-Lichinga – Phase 1 | Niassa Province | 46,8 | |

[1] AfDB, "Speech by Akinwumi A. Adesina, President of the African Development Bank, at the "Feed Africa: Food Sovereignty and Resilience" Summit, January 25-27, 2023 Dakar, Senegal", January 25, 2023: https://www.afdb.org/fr/news-and-events/speeches/discours-prononce-par-akinwumi-adesina-president-de-la-banque-africaine-de-developpement-au-sommet-nourrir-lafrique-souverainete-alimentaire-et-resilience-du-25-au-27-janvier-2023-dakar-senegal-58442

[2] AfDB, "High level roundtable: Closing the Financing Gap", January 26, 2023, https://www.youtube.com/live/PCWrkqk1g0Y?feature=share&t=28106

[3] AfDB, "Financial Report 2022", 2023, https://www.afdb.org/fr/documents-publications/rapport-annuel, p. 89.

[4] The breakdown of AfDB loans and grants is as follows: West Africa (28.2%), East Africa (24.7%), Southern Africa (18.5%), North Africa (13.2%), Central Africa (10.5%), multi-regional (4.8%) (AfDB, “Annual Report 2022”, 2023, https://www.afdb.org/fr/documents-publications/rapport-annuel , p. x, 7, 36)

[5] AfDB, "Annual Report 2022", 2023, https://www.afdb.org/fr/documents-publications/rapport-annuel, p. 8

[6] See: https://ejatlas.org/

[7] Reine Fadonougbo Baimey, « Women resisting African Development Bank projects demand reparations », WoMin, May 25, 2023, https://womin.africa/women-resisting-african-development-bank-projects-demand-reparations/

[8] AfDB, “Closing Remarks by Mr. Akinwumi A. Adesina, President of the African Development Bank Group - “Feed Africa: Food Sovereignty and Resilience” Summit. January 27, 2023 - Dakar, Senegal, January 27, 2023 : https://www.afdb.org/fr/news-and-events/speeches/allocution-de-cloture-prononcee-par-m-akinwumi-adesina-president-du-groupe-de-la-banque-africaine-de-developpement-sommet-nourrir-lafrique-souverainete-alimentaire-et-resilience-27-janvier-2023-dakar-senegal-58582. Les Pactes peuvent être consultés ici: https://www.afdb.org/en/dakar-2-summit-feed-africa-food-sovereignty-and-resilience/compacts

[9] African Union, « Draft. Decisions, declaration, resolution and motion », 36e Assembly, February 18-19, 2023 : https://www.afdb.org/sites/default/files/documents/resolutions_36th_ordinary_session_african_union_assembly_19_february_2023.pdf

[10] This estimate excludes Cape Verde, Togo and Zimbabwe given the lack of budget in these Pacts.

[11] Africa Check, “Electricity Access and Arable Land in Africa: Two Macky Sall Claims Examined”, October 27, 2022, https://africacheck.org/fr/fact-checks/articles/acces-lelectricite-et-terres-arables-en-afrique-deux-affirmations-de-macky

[12] AfDB, « Tanzania: Country Food and Agriculture Delivery Compact », 2023, p. 17 https://www.afdb.org/fr/documents/tanzania-country-food-and-agriculture-delivery-compact

[13] A recent critical analysis of PPPs can be viewed here: Eurodad, « History rePPPeated II - Why public-private partnerships are not the solution », December 1, 2022, https://www.eurodad.org/historyrepppeated2

[14] See: WRM, "Help us stop the spread of oil palm monocultures in Gabon!" », September 13, 2019, https://www.farmlandgrab.org/post/view/29152-aidez-nous-a-stopper-la-progression-des-monocultures-de-palmier-a-huile-au-gabon; https://www.wrm.org.uy/fr/articles-du-bulletin/gabon-les-communautes-face-aux-engagements-de-deforestation-zero-dolam

[15] AfDB, « Communique of the Fifty-Eighth Annual Meeting of the Board of Governors of the African Development Bank (AfDB) and the Forty-ninth Annual Meeting of the Board of Governors of the African Development Fund (ADF) Held On 22nd – 26th May 2023 », May 26, 2023, https://www.afdb.org/en/documents/communique-fifty-eighth-annual-meeting-board-governors-african-development-bank-afdb-and-forty-ninth-annual-meeting-board-governors-african-development-fund-adf-held-22nd-26th-may-2023

[16] AfDB, « Feed Africa: food sovereignty and resilience. Day 2 », January 26, 2023, https://www.youtube.com/live/PCWrkqk1g0Y?feature=share&t=4945;AfDB, "Dakar 2 Summit: Development Partners to Invest $30 Billion to Boost Food Production in Africa", January 27, 2023 : https://www.afdb.org/fr/news-and-events/press-releases/sommet-dakar-2-les-partenaires-au-developpement-vont-investir-30-milliards-de-dollars-pour-stimuler-la-production-alimentaire-en-afrique-58599; BAD, « International support for Africa’s plan to transform agriculture hits $50 billion », March 3, 2023, https://www.afdb.org/en/news-and-events/international-support-africas-plan-transform-agriculture-hits-50-billion-59468; « World Bank president nominee pledges change », The Independent, March 15, 2023, https://www.independent.co.ug/world-bank-president-nominee-pledges-change/. Netherlands International Cooperation also announced support of $30 million for the AfDB's African Emergency Food Production Facility.

[17] CADTM, “Afrique : le piège de la dette et comment en sortir”, 2022, https://www.cadtm.org/Afrique-le-piege-de-la-dette-et-comment-en-sortir

[18] Frédéric Miezan, « History of the African Development Bank and its contribution to the development of Côte d'Ivoire 1963-2005 », Paris : Société française d’histoire des outre-mers, 2012, https://www.persee.fr/docAsPDF/sfhom_0000-0003_2012_mon_8_1_912.pdf

[19] This process took place under the chairmanship of Wila Mung’omba, who had played a key role in the privatization of mines in Zambia. See: Frédéric Miezan, "History of the African Development Bank and its contribution to the development of Côte d'Ivoire 1963-2005", Paris: French Society for the History of Overseas, 2012, https://www.persee.fr/docAsPDF/sfhom_0000-0003_2012_mon_8_1_912.pdf; and Damien Millet, « La dette de l’Afrique aujourd’hui », CADTM, March 29, 2005, https://www.cadtm.org/spip.php?page=imprimer&id_article=1261.

[20] See: AfDB, “Lending Instruments», s/d, https://www.afdb.org/fr/about-us/corporate-information/financial-information/lending-instruments; Rachel Wynberg, Gaia, GRAIN, « Privatization of the means of survival: The commercialization of Africa's biodiversity, May 25, 2000, https://grain.org/fr/article/61-privatisation-des-moyens-de-survie-la-commercialisation-de-la-biodiversite-de-l-afrique

[22] AfDB, “Equity Acquisitions in Africa. The role of the African Development Bank. A key player in the development of capital markets”, 2021, https://www.afdb.org/sites/default/files/news_documents/private_equity_in_africa_-_the_role_of_the_afdb_2021_-_french.pdf

[24] The amount in the currency used by the AfDB (AU) is: 13,891.17 billion. The exchange rate in June 2023 can be viewed here : https://www.afdb.org/en/documents/june-2023-exchange-rates

[25] AfDB, “Annual Report 2022», 2023, https://www.afdb.org/fr/documents-publications/rapport-annuel, p. 81, 82

[26] AfDB, “Annual Report 2022 », 2023, https://www.afdb.org/fr/documents-publications/rapport-annuel

[27] The Bank claims to have carried out between 2006 and 2014, 198 operations in agriculture and agro-industry for an amount of 6.3 billion dollars. (ADB, « Feed Africa. Strategy for agricultural transformation in Africa 2016 – 2025 », 2016, https://www.afdb.org/fileadmin/uploads/afdb/Documents/Policy-Documents/Feed_Africa-Strategy-En.pdf; « Annual report 2021: highlights », July 19, 2022, https://www.afdb.org/en/documents/african-development-bank-group-annual-report-2021-highlights).

[28] AfDB, "Questions and Answers: The Dakar 2 Summit", 2023, https://www.afdb.org/fr/sommet-dakar-2-nourrir-lafrique-souverainete-alimentaire-et-resilience/questions-et-reponses-le-sommet-dakar-2

[30] AfDB, “Feed Africa. Strategy for the transformation of African agriculture 2016 - 2025», 2016, https://www.afdb.org/fileadmin/uploads/afdb/Documents/Policy-Documents/Feed_Africa_-_Strategie-Fr.pdf

[31] AfDB, « Questions and answers : lL Sommet Dakar 2 », 2023, https://www.afdb.org/fr/sommet-dakar-2-nourrir-lafrique-souverainete-alimentaire-et-resilience/questions-et-reponses-le-sommet-dakar-2

[32] AfDB, "TAAT, AfDB's new strategy to ensure 513 million tons more food production", October 20, 2017, https://www.afdb.org/fr/news-and-events/afdbs-agricultural-transformation-strategy-to-guarantee-513-million-tons-of-additional-food-production-17463

[33] See: "African Development Bank (ADB): Syngenta case, a big potato in the re-election of President Adesina", Orishas Finance, August 16, 2020, https://www.orishas-finance.com/actualite/1898?lang=fr; et Vincent Duhem, « AfDB: What’s in the confidential report exonerating Adesina », The Africa Report, May 11, 2020, https://www.theafricareport.com/27758/afdb-whats-in-the-confidential-report-exonerating-adesina/

[34] See: TAAT, « TAAT’s deployment model offers hope for mitigating Fall Armyworm infestation », May 10, 2023, https://taat-africa.org/news/taats-deployment-model-offers-hope-for-mitigating-fall-armyworm-infestation/; TAAT, « Farmers expect bumper harvest as TAAT Maize technologies tackle Fall Armyworm », December 14, 2019, https://taat-africa.org/news/farmers-expect-bumper-harvest-as-taat-maize-technologies-tackle-fall-armyworm/; et « TAAT Updates 2018», 2018, https://taat-africa.org/wp-content/uploads/2019/09/REVISED_TAAT_update25-june2019E.pdf

[35] See: SAFCEI, « African faith communities tell Gates Foundation, “Big farming is no solution for Africa" », August 4, 2021, https://grain.org/en/article/6706-african-faith-communities-tell-gates-foundation-big-farming-is-no-solution-for-africa; GRAIN, «How the Gates Foundation is pushing the food system in the wrong direction,” June 28, 2021, https://grain.org/fr/article/6696-comment-la-fondation-gates-pousse-le-systeme-alimentaire-dans-la-mauvaise-direction; JVE Ghana et GRAIN, «AGRA endorses and consolidates the climate crises of today and tomorrow,” September 5, 2019 , https://grain.org/fr/article/6320-l-agra-enterine-et-consolide-les-crises-climatiques-d-aujourd-hui-et-de-demain

[36] AfDB, "Speech by Mr. Akinwumi Adesina, President of the African Development Bank Group - Knowledge Exchange hosted by YARA - Oslo", September 29, 2022, https://www.afdb.org/fr/news-and-events/speeches/discours-de-m-akinwumi-adesina-president-du-groupe-de-la-banque-africaine-de-developpement-echange-de-connaissances-organise-par-yara-oslo-le-29-septembre-2022-55156

[37] Groupe ETC, «African Development Bank Group: Dakar 2 Summit», January 26, 2023, https://www.etcgroup.org/fr/content/groupe-de-la-banque-africaine-de-developpement-sommet-dakar-2

[38] See for example : Frederic Mousseau and Andy Currier, « The African Development Bank Must Work for Africans, Not Agrochemical Corporations », Oakland Institute, September 15, 2022, https://www.oaklandinstitute.org/blog/african-development-bank-agrochemical-corporations; GRAIN et IATP, « A corporate cartel fertilizes food inflation», May 23, 2023, https://grain.org/fr/article/6990-un-cartel-d-entreprises-fertilise-l-inflation-alimentaire

[39] AfDB, « Nigeria - « Dangote Industries Limited » - (Refinery and fertilizer production projects) », s/d, https://projectsportal.afdb.org/dataportal/VProject/show/P-NG-FD0-003?lang=fr

[40] The average application in sub-Saharan Africa is said to have increased from 6 kg/hectare in 2000 to 17 kg in 2017 (AfDB and UNECA, "Promotion of fertilizer production, cross-border trade and consumption in Africa", 2018, https://www.afdb.org/fileadmin/uploads/afdb/Documents/Generic-Documents/Study__sponsored_by_UNECA___AFFM__on_promotion_of_fertilizer_production__cross-border_trade_and_consumption_in_Africa.pdf).

[41] The countries targeted are: Nigeria, Tanzania, DRC, Ghana, Ivory Coast, Ethiopia, Zambia, Kenya, Mozambique, Niger, Burkina Faso, Malawi, Senegal, Zimbabwe and Uganda (AfDB, « Africa Fertilizer Financing Mechanism (AFFM) – Strategic Plan 2022-2028 », May 25, 2022, https://www.afdb.org/en/documents/africa-fertilizer-financing-mechanism-affm-strategic-plan-2022-2028).

[45] « AfDB Approves $11.7 Million To Facilitate Access To Fertilizers For African Farmers », Business Today, May 18, 2023, https://businesstodayng.com/afdb-approves-11-7-million-to-facilitate-access-to-fertilizers-for-african-farmers/

[46] Tom Collins, « Time for Africa to feed itself – Dakar 2 summit takes Africa’s food agenda forward », Africa Business, February 28, 2023: https://african.business/2023/02/resources/time-for-africa-to-feed-itself-dakar-2-summit-takes-africas-food-agenda-forward

[47] AfDB, « Partnership for Agro-Industrialization in Africa (SAPZ) », September 20, 2021, https://www.afdb.org/sites/default/files/documents/2021_09_20_partnership_for_agro-industrialization_in_africa.pptx

[48] AfDB, « AfDB Research Study - Prospects for the Development of Special Agro-Industrial Processing Zones (SAPZs) in Africa: Lessons from Experience », July 2021, https://www.afdb.org/fr/documents/etude-de-recherche-de-la-bad-perspectives-de-developpement-des-zones-de-transformation-agro-industrielle-speciales-sapz-en-afrique-lecons-de-lexperience

[49] Collectif TANY, « But what is happening in Bas-Mangoky in Madagascar?», October 15, 2022, https://www.farmlandgrab.org/post/view/31192-mais-que-se-passe-t-il-dans-le-bas-mangoky-a-madagascar. This was hardly the first time that loans had helped facilitate pro-agribusiness policies. Already in 2005, a multi-million dollar loan for rural reconstruction in the Democratic Republic of Congo was conditional on the approval of a seed law (GRAIN, "Seed Laws in Africa: A Red Carpet for Private Companies", July 8, 2005, https://grain.org/fr/article/526-lois-sur-les-semences-en-afrique-un-tapis-rouge-pour-les-societes-privees).

[50] See : CNUCED, « World Investment Report 2019 », June 12, 2019, https://unctad.org/webflyer/world-investment-report-2019; et https://gasez.org/about.

[51] « AfDB Approves $11.7 Million To Facilitate Access To Fertilizers For African Farmers », Business Today, May 18, 2023, https://businesstodayng.com/afdb-approves-11-7-million-to-facilitate-access-to-fertilizers-for-african-farmers/

[52] Land Tenure and Development Technical Committee, « Special economic zones and land tenure. Global trends and local impacts in Senegal and Madagascar », September 2022, https://www.foncier-developpement.fr/publication/special-economic-zones-and-land-tenure-global-trends-and-local-impacts-in-senegal-and-madagascar/

[53] Action contre la faim, CCFD – Terre solidaire, Oxfam France, « The impasse of agricultural growth poles” 2017, https://ccfd-terresolidaire.org/wp-content/uploads/2017/06/rapport_pcaa_exe_ok.pdf

[54] Inter-réseaux développement rural, « Agricultural growth poles: the panacea to the ills of African agriculture? », December 2016, https://www.inter-reseaux.org/wp-content/uploads/bds_no24_poles_de_croissance.pdf

[55] Etienne Lankoandé, « Bagré pole, ten years later", Lefaso.net, December 10, 2020, https://www.farmlandgrab.org/post/view/30003-bagre-pole-dix-ans-apres

[56] Action contre la faim, CCFD – Terre solidaire, Oxfam France, « The impasse of agricultural growth poles », 2017, https://ccfd-terresolidaire.org/wp-content/uploads/2017/06/rapport_pcaa_exe_ok.pdf

[57] A list of AfDB-funded and non-funded agro-industrial zones and parks can be found here: AfDB, "AfDB Research Study - Prospects for the Development of Special Agro-Industrial Processing Zones (SAPZs) in Africa: Lessons from Experience", July 2021, https://www.afdb.org/fr/documents/etude-de-recherche-de-la-bad-perspectives-de-developpement-des-zones-de-transformation-agro-industrielle-speciales-sapz-en-afrique-lecons-de-lexperience, p. 108

[58] See: AfDB, "Questions and Answers: The Dakar 2 Summit », 2023, https://www.afdb.org/fr/sommet-dakar-2-nourrir-lafrique-souverainete-alimentaire-et-resilience/questions-et-reponses-le-sommet-dakar-2; et AfDB, “Special Agro-Industrial Processing Zones Program in Nigeria: 10 Quick Facts to Know», October 28, 2022, https://www.afdb.org/fr/news-and-events/programme-des-zones-speciales-de-transformation-agro-industrielle-au-nigeria-10-faits-en-bref-savoir-55889

[59] See: AfDB, "Senegal - Central Agro-Industrial Processing Zone Project - Project Appraisal Report", October 28, 2022, https://www.afdb.org/fr/documents/senegal-projet-de-zone-de-transformation-agro-industrielle-du-centre-rapport-devaluation-de-projet; and "Senegal: a loan of more than 63 million euros for the establishment of an agropole in four regions of the Center of the country", October 26, 2022, https://www.afdb.org/fr/news-and-events/press-releases/senegal-un-pret-de-plus-de-63-millions-deuros-pour-la-mise-en-place-dune-agropole-dans-quatre-regions-du-centre-du-pays-55766

[60] AfDB, « Partnership for Agro-Industrialization in Africa (SAPZ) », September 20, 2021, https://www.afdb.org/sites/default/files/documents/2021_09_20_partnership_for_agro-industrialization_in_africa.pptx

[61] Martin Mateso, « Farmland: African peasants give way to multinational corporations », GeopolisTV, April 14, 2017, https://www.farmlandgrab.org/post/view/27059-terres-agricoles-les-paysans-africains-seffacent-face-aux-multinationales

[62] AfDB, “Development Program for the Special Agro-Industrial Processing Zone of the Koulikoro and Peri-Urban Regions of Bamako (PDZSTA-KB). Evaluation Report, December 2019, https://projectsportal.afdb.org/dataportal/VProject/show/P-ML-AAG-004?lang=fr

[63] See also: "Agropoles: a panacea for African agriculture?" », Afrik.com, 8 décembre 2017, https://www.farmlandgrab.org/post/view/27727-les-agropoles-une-panacee-pour-lagriculture-africaine

[64] See for example: GRAIN, “A new green revolution for Africa? », 2007, https://grain.org/fr/article/137-une-nouvelle-revolution-verte-pour-l-afrique; and Sayouba Traoré, « Industrial Agriculture and Land Grabbing in Africa”, RFI, July 15, 2017, https://www.farmlandgrab.org/post/view/27297-lagriculture-industrielle-et-laccaparement-des-terres-en-afrique

[65] GRAIN, « Food sovereignty is the only solution to climate chaos for Africa”, July 31, 2019, https://grain.org/fr/article/6297-la-souverainete-alimentaire-est-la-seule-solution-au-chaos-climatique-pour-l-afrique

[66] Civil society increasingly denounces public banks like the AfDB. See for example: "Development banks are not for financing agribusiness", October 17, 2021, https://grain.org/fr/article/6756-les-banques-de-developpement-n-ont-pas-vocation-a-financer-l-agrobusiness