“Agro is pop, agro is tech, agro is everything” states a popular slogan in adverts broadcast on Brazil's largest TV channel since 2016. Financed by agribusiness, these advertisements portray a virtuous cycle, showcasing images of contented rural workers amidst soybean, corn, cotton, and sugar cane plantations, as well as happy urban families. They are all content because they can feed, clothe themselves, and fuel their cars, thanks to the agro-industry.

As part of the marketing campaign, mainstream media echoes the mantra that the sector is said to account for close to 25% of Brazil's GDP, which would make it a major source of national wealth.

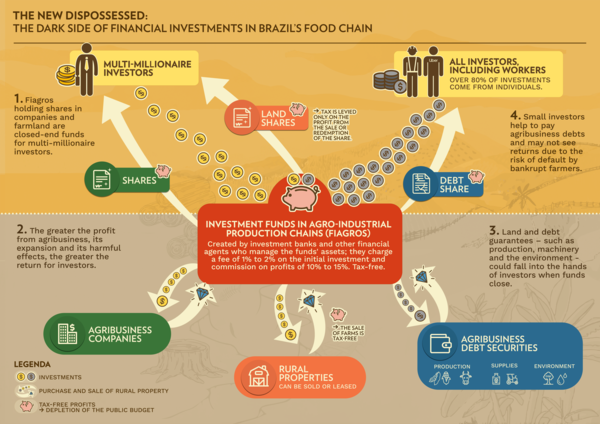

This triumphalist image of agribusiness aligns perfectly with the strategy of the relatively new Investment Funds in Agro-Industrial Production Chains, known as Fiagros, which promise that anyone can take a piece of the sector's wealth by becoming an agribusiness "partner". Created in 2021, Fiagros offer shares from as little as USD 2 (Brazilian Real - BRL10), giving investors a tax-free return that is generally above the country’s interest rates (on average 12% per year).[1]

This phenomenon is not limited to Brazil. In Mexico, agritech companies offering advice on agricultural investments, mainly in the production of berries, agave and avocado for export, have multiplied in recent years. Many young investors in the cities are now using apps on their mobile phones to enter into “sowing pools” to become "owners of their own plot of green gold" or “co-owners of assets, benefiting from the income generated”. However, they remain far removed from the consequences of this easy profit, which include illegal grabbing of land and water resources and slave-like labour exploitation.[2] [3]

Even without the current drive to popularise financial investments, Argentina introduced thousands of hectares of mainly GM soybean during the 2000s, priced in dollars on the capital markets, in order to guarantee annual returns for investors in pools de siembra (sowing pools), which reached 38% in 2008.[4]

The system created a new figure, the "agricultural manager", who was now able to organise Argentinian production from offices anywhere in the world, using resources raised through joint investor funds. These types of funds increased by 270% between 2004 and 2008, contributing to a quarter of the country's arable land falling into the hands of joint-stock companies.[5] [6] From 2008, the serious crisis in Argentina scared off investors, significantly reducing the activity of the pools de siembra. Despite the current ultra-liberal policies of recently-elected president Javier Milei who promises "All power to the pools" and to financial capital, the country is witnessing significant protests from broad sectors of the population - ranging from national agribusiness to peasants, Indigenous peoples to members of the armed forces - against the sale of national wealth and the foreign ownership of land.[7]

In the United States, a very similar fund to the current Fiagros in Brazil was put on the table at the end of the 1970s, known as the AG-Land Trust. This fund intended to purchase land with the aim of inflating its value for profitable resell, to then distribute tax-free capital gains to shareholders - in this case, institutional investors. The initiative faced strong opposition from farmers and was blocked by Congress and subsequently by various anti-corporate state agricultural laws. It was seen as a Wall Street strategy to create financial bubbles in land prices, which would result in a majority of dispossessed farmers, subjected to paying high rents to a small elite of financial investors.[8]

However, from the 1980s, several instruments began to facilitate the acquisition of land by institutional investors in the US, such as investment funds in forestry and agricultural land, the so-called REITs (Real Estate Investments Trust). By March 2023, the value of agricultural land controlled or owned by institutional investors in the country rose to over USD 15 billion. This was an increase of 66% compared to 2008, when this land began to be used more as a financial asset aimed at investor profits, yielding a 9.64% return in 2022.[9] By March 2023, the total market value of Timberland Properties, a major global player in the real estate investment sector, was over USD 24 billion, with a return of 12.9%.[10] Meanwhile, the number of family farms in 2023 in the US was nearly four times lower than in 1935, dropping from 6.8 million farms to 1.8 million.[11]

Brazil may be following suit. Three years after launching the first Fiagros in the country, experts argue that the results of this scheme could be catastrophic.[12] Using the slogan of "agro is pop, agro is tech, agro is everything", financial and agribusiness agents are trying to sell a pig in a poke, to cover up the sector's economic, ecological and social bankruptcy, in addition to the high risk of these investments.

By launching a private loan mechanism to attract large swathes of the population, this thriving sector is actually revealing that it can only sustain itself by issuing debt upon debt, by relying on state subsidies and the constant flattening of production costs, which means the exploitation of labour and the grabbing of land, water and other natural resources.[13]

With this idea that everyone can be an “agro partner”, these funds are trying to snatch people's savings to share out the sector's risks and debts and finance the expansion of the agro-industry and everything that historically goes with it. Seizing people's savings to finance more land enclosures, exploitation of labour and grabbing of natural resources may be one of the most perverse consequences of this new agribusiness financial strategy.

Debt partners

Currently, Brazil has three types of Fiagros: 1) Fiagro-FIP investing in corporate participation, mainly in shares in agribusiness companies; 2) Fiagro-FIDC investing in credit rights, i.e. the sector's debt instruments ("agribusiness bonds"); and 3) Fiagro-FII investing in real estate assets such as rural real estate, real estate credit rights and agribusiness credit rights.

While Fiagro and land Fiagro shares are restricted to millionaire investors, debt Fiagro is open to everyone. Fiagro-FII, with its wider range of asset types, is the most in demand, with 60 funds and 69,000 accounts, accounting for almost half of Fiagros' total assets (USD 3.331 billion). By September 2023, 66% of their investments were in debt securities and 20% in real estate, according to the CVM Agribusiness Bulletin for September 2023.

Since the change in the law on agribusiness bonds in 2020 and the creation of the Fiagros in 2021, the volume of the debt market and agribusiness funding instruments on the financial market has more than doubled, according to the Ministry of Agriculture's Agribusiness Private Finance Bulletin.

Agribusiness debt securities dominate the Fiagros' portfolios. The main one, the Agribusiness Receivables Certificate (CRA), issued only by securities companies, represents 55% of the funds' total assets, according to the CVM. With a return linked to the high interest rates in the country, short-term redemption of the amount invested and tax-free monthly dividend payments, it has become the most popular option. However, it is also the one that involves the greatest risk, as it depends on payments from farmers who, with soybean and maize prices falling and input costs rising, are beginning to delay payments and declare default on debts to the funds, or rather, to the new agro (debt) "partners".[14]

For example, in May 2023 Usina Ester S.A, one of the sugar mills issuing CRAs that make up part of the Fiagros XPAG1 and XPCA11 portfolios managed by XP Investimentos, filed for bankruptcy due to debts over BRL 650 million (USD 130 million), jeopardising the monthly payment of the CRAs that constitute the funds' assets.[15] Despite the fact that the Funds requested the seizure of part of the production stored by the plant and reached a judicial agreement for payment, the profitability of the quotas was compromised. XPCA11, with more than 100,000 investors, which paid a return of 176% of the interest-linked index in February 2023, delivered a return of 127% in June 2023.[16]

Democratising finance or snatching people's savings?

By March 2024, 98 Fiagros were registered with the Brazilian Securities and Exchange Commission (Comissão de Valores Mobiliários, CVM), accumulating a net worth of USD 6.8 billion, spread over 690,000 accounts, according to data from the Brazilian Financial and Capital Markets Association (Anbima).[17] Of this total, only 43 funds, totalling USD 4.1 billion, are listed on the B3 Stock Exchange, with a total of 490,000 investors. Ninety-four per cent of these stock market investors are individuals, accounting for 83% of the investment volume.[18]

This means that over half of the funds, with 60% of the total wealth, are not listed on the stock exchange. They are held by only 29% of investors, about which nothing is known, given that there is no obligation to share monthly reports. Only those Fiagros that invest in the purchase of shares for a stake in agribusiness companies (Fiagro-FIP) are excluded from listings on the stock exchange. Although they account for almost 40% of the Fiagros' total assets (USD 2.7 billion), there are only 73 investors. As this type of fund can invest up to 20% of its capital in assets abroad, this Fiagro could, behind the scenes, be an important mechanism for remitting profits and dividends out of the country without paying taxes.

While these closed-end funds particularly benefit super-rich families, who can set up a fund just to avoid paying taxes, the public offering of shares with high returns , tax-free, also makes the Fiagros an attractive and accessible investment option for the general public.[19]

However, high profitability always goes hand in hand with high risk. Fiagros are considered a risky investment, since their wealth is tied up in assets that are susceptible to external factors, such as the climate, pests, crop failures, credit and insurance, land ownership rights, problems with logistics and transport infrastructure. For this reason, the “democratisation” of investments aims to attract the savings of individuals from all walks of life to help the funds gain momentum and create sufficient assets to dispel the misgivings of larger investors, such as pension and investment funds.

Fiagros have been paying significant dividends, an average of 1.13% per month, according to a report from November 2023.[20][21] This profitability is due to the fact that the majority of the funds' assets are made up of debt securities that pay interest at 11.25% per year.[22] Therefore, until now, Fiagros have ridden the wave of the highest real interest rates in the world, while rural producers roll over their debts at a stratospheric cost, extending the vicious cycle of indebtedness in the sector.

Although the capital market and financial investments are dominated by the richest segment of the population, the number of investors in Brazil is increasing. There are now 60 million investors, with an increase in investors across all social classes, especially class C - households earning between USD 565 and USD 1,383 – which is up from 29% to 36%.[23] The so-called financialisation of the economy is betting on this gradual transfer of people's savings from savings accounts (which are the most widely used in the country today) and public pensions (the source of income for 90% of the retired population) to financial mechanisms such as investment funds.

The heavy marketing of "Agro is everything" has been one of the main mechanisms for popularising the capital market, with influencers on social media and YouTube showing viewers how to identify the type of investment to invest simply and quickly using mobile phone apps, in just a few clicks.[24] Torn between investing their savings in public pensions, savings accounts or even their own businesses, many workers have fallen prey to the temptation of seeking quick returns through these financial mechanisms.

The biggest increase in the number of investors occurred among people living in the Brazilian Cerrado, from 33% to 43% of the total population, which is precisely where the major “agribusiness cities” are located.[25] Those who are now placing their savings in agribusiness debt securities and Fiagros shares could well be the children or grandchildren of the 30% of the displaced rural population who, between 1980 and 2010, had to leave their homes to make way to soybean monoculture.[26]

click on image to zoom

click on image to zoom Land Fiagros: concentrating ownership through financialisation

Although rural property represents only 17% of the assets held by Fiagros, the volume of investments in land almost doubled from June to September 2023, from USD 350.72 million to USD 584.53 million.[27] The so-called "Land Fiagros", with 100% of their investments in agricultural land, are generally restricted to professional investors (with investments of over USD 2 million) and qualified investors (over USD 200,000), with the aim of increasing the value of the land in the medium and long term - eight to ten years - and paying annual dividends.

In addition to the tax exemption on income, the law also allows for the non-payment of taxes when rural property is sold to these funds. Taxes are only paid on the profit from the resale of each share on the capital market, and not on the entire property when it is sold. Large landowners can set up these funds as a strategy to transfer inheritance without paying tax or even to simulate land deals in order to evade debts.

Worse still, this tax waiver for land deals via Fiagros could potentially concentrate ownership of land in the hands of these funds, changing the very logic of land price composition. In addition to the assessment of specific factors such as soil quality, topography, the presence of water and infrastructure, the price is also influenced by the interests of this new category of land investors and the dynamics of buying and selling shares.

In order to pursue greater profitability, the funds began leasing land to producers and companies that specialise in pursuing crops with a higher market value and quick returns, usually commodities traded in dollars on the futures markets (not food), and now not just agricultural commodities, but also "agri-environmental" ones. The leases aim to increase the value of the land until it is sold, with pre-emptive purchase rights for the lessee, and the distribution of profits to investors. Fiagros, however, can be used as mechanisms to create speculative bubbles in prices, such as by buying and selling land to each other. (See Box 2 Green Fiagro: financial expertise in land inflation)

Green Fiagro: profiting from pasture recovery

In 2023, the first Green Fiagro was created: the AGBI III Carbon Fiagro FIP fund. Managed by AGBI real assets, with the status of "green fund" or "art.9 fund" under the Paris Agreement, it followed the criteria of the Climate Bonds Initiative (CBI) and the Sustainable Finance Disclosure Regulation (SFDR), used as a standard in the European Union. [28]

The aim of the fund is to recover pastures by applying questionable carbon farming techniques and technologies in order to generate and commercialise carbon credits certified by Verra – a major global carbon certification programme, linked to highly controversial carbon projects.[29] [30]

The soil regeneration strategy for areas of degraded pasture is more profitable than environmental, as it ends up intensifying soil degradation and deforestation, while inflating the price of land. On the one hand, the expansion of agricultural monocultures or trees planted on areas of pasture that have already been "cleared" is much more cost-effective than cutting down and clearing forests. [31]

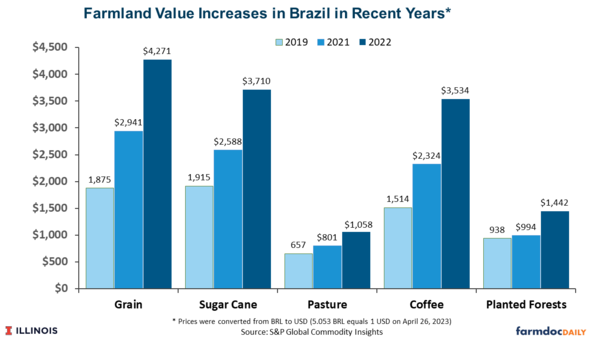

On the other hand, it pushes livestock farming onto forests and native vegetation. In addition to quadrupling the value of land by converting low-yielding pastures into arable land (see graph “Farmland value increases in Brazil in recent years”), this focus on the "green modernisation" of farmland by the funds aims to inflate the price of land even further.

Another two of the management company's funds that carried out pasture recovery sold two farms with an increase in value of 451% in eight years and 517% in seven years.[32] Even with the price of beef at an all-time low and land deals stagnating compared to previous years, pastureland was valued at four times more than arable land in Brazil in 2023.[33]

With this trend in mind, it is foreseeable that Green Fiagros will increasingly acquire degraded land, especially considering Brazil's commitment to "recover" 30 million hectares between 2020 and 2030 under the Low Carbon Agriculture+ Plan (Plano Agricultura de Baixo Carbono+).

The most profitable Fiagro shares are those investing in farmland, also called "Land Fiagros". The return on these shares depends on the value of the leases, generally linked to the value of a sack of soybean per hectare, which also varies according to the availability of water for irrigation.[34] This demonstrates both the strong link between the price of land and agricultural commodities in producing regions, as well as the indirect pricing of water by financial agents, which in turn also has an impact on the value of leases, land and now also fund share prices.

These land Fiagros include the three managed by XP investimentos, which together total 35,000 hectares in the Matopiba region, leased to SLC Agrícola mainly for the production of soybean, along with maize, cotton and brachiaria grass.[35] The company is the largest producer of soybean in the country, and not by chance; it is also responsible for the deforestation of at least 30,000 hectares of native vegetation in the Cerrado. [36] Two of these farms are located in Correntina in Bahia, a scene of the most intense water conflicts in the country’s history, marked by the escalation of water grabbing by corporations and irrigation projects.[37]

While the profitability of shares is susceptible to the likelihood of default on debt payments, the same is not true of non-economic violence. Despite the "green finance" agenda, in practice capital markets and investors are chasing the highest returns, and this is often accompanied by deals involving land grabbing, deforestation, illegal water extraction or the use of slave labour. (See Table "Land Fiagros: land and water grabbing as well as deforestation")

Land property agents believe that the current period is a great opportunity to buy cheap land. After an intense rise in value over the last three years, with average land prices for grain production rising by 128%, this curve stagnated in 2023.[38] The loss of profitability for farmers due to the commodities slump and the increase in production costs puts their land at risk. This situation could lead to the next period of concentrated land ownership in the hands of the Fiagros and their millionaire investors, taking discounted land away from indebted farmers or those lacking the capital to maintain it.

Source: Colussi J., G. Schnitkey, N. Paulson, and J. Baltz. “Farmland Prices in Brazil More than Doubled in the Last Three Years.” farmdoc daily (13): 79, Department of Agricultural and Consumer Economics, University of Illinois at Urbana-Champaign, April 28, 2023.

The Brazilian government is studying the creation of “Fiagros for land in debt”, where on the one hand creditors - retailers, suppliers, banks, trading companies - become fund partners, and on the other, the farmer transfers the farm and becomes a Fiagro tenant. The debts would be paid back through production until, at the end of the repayment period, the farmer would have the right to buy back the shares and recover the property. But getting their property back is unlikely if the period of land concentration persists, facilitating the creation of speculative bubbles in land prices.[39]

Behind the veil of “democratising” finance and property, the financialisation of land tends to cause precisely the opposite effect: further concentration of capital and land at the hands of financial elites.

Land grabbing and shielding for investors, including foreigners

To provide investors with security, agribusiness debt instruments and Fiagros have privileged payment guarantees. With the creation of the so-called "segregate estate", the Brazilian Agro Law makes it possible to separate all or parts of rural estates in proportion to the debt, as a guarantee to specifically pay off the obligations of agribusiness companies. If the debt is not repaid, the land covered by the debt must be transferred directly into the creditor's name at the land registry office, without the need for legal action. Moreover, if the creditor is a foreign investor, the agro securities law authorises the transfer of land to foreigners in the event of debt enforcement, regardless of the limits on access to land by foreigners. This circumvents the law that limits foreigners' control of land in the country.[40]

The land allocated for the specific payment of agribusiness debts cannot be the object of a sale or purchase, donation, judicial recovery, or bankruptcy proceedings, nor can it be used to pay other debts, with the exception of tax, pension and labour debts of the indebted producer or company. Therefore, although this mechanism is in place to shield the land in favour of paying investors, the state and workers retain preference in the list of creditors, which could leave new shareholders in the lurch.

It should also be emphasised that these lands assigned as collateral for debts may in fact be public and communal land that has been grabbed.[41] As reported by various organisations, Brazil has permitted the widespread legalisation of historic land grabbing of public lands, particularly after the institutional coup of 2016, with the so-called Land Grabbers’ Act (Lei da grilagem), which has been replicated by the states, including Matopiba.[42] This means that rather than the seizure of private assets, the failure of many farmers to pay up could lead to the confiscation of public land - the land belonging to the entire population - and land grabbed from local communities. Consequently, this land could potentially end up in the possession of these financial entities.

Greenwashing debts and environmental services as “rural products”

The new trend among Fiagros is to expand their portfolio to activities considered of low environmental impact, by buying the assets or debts of bioenergy companies or those that use "regenerative" farming practices, such as the recovery of pastures or the industrial planting of trees.[43]

The new trend among Fiagros is to expand their portfolio to activities considered of low environmental impact, by buying the assets or debts of bioenergy companies or those that use "regenerative" farming practices, such as the recovery of pastures or the industrial planting of trees.[43]

The new trend among Fiagros is to expand their portfolio to activities considered of low environmental impact, by buying the assets or debts of bioenergy companies or those that use "regenerative" farming practices, such as the recovery of pastures or the industrial planting of trees.[43]This interest in so-called "green bonds" goes hand in hand with the global movement to "greenwash" the image of corporations and financial agents, while also taking advantage of the trend towards the increasing value of these "nature-based" assets. Legal disputes are raging between countries over the definition of ownership. In other words, over who owns forest and soil carbon credits and other environmental services, such as water conservation.

Brazil’s agribusiness securities law, amended in 2022, began to consider the provision of environmental services on farms as a new type of "rural product", authorising the issue of debt securities on formerly common goods - which could not be appropriated, negotiated or enforced by debt, like any other commodity.[44] They started to consider the following to be “rural products”:

- “services” for conservation and recovery of native forests

- reduction of deforestation

- water and soil conservation

- reducing or maintaining emissions

- increasing forest carbon stocks, among other ecosystem benefits, if certified by a third party.[45]

This means excluding the majority of current and future generations from access to the environmental standards required for a decent quality of life, and the introduction of environmental services as collateral for rural producers' debts. This could set a legislative precedent in other countries where agribusiness is considered a supplier of carbon credits and other environmental services.

Furthermore, the social and environmental commitment of agribusiness is catastrophic, and the funds are key mechanisms for greenwashing this track record. Worse still, it perversely links the expected income of these unsuspecting new investors to the expansion of the agricultural frontier and everything that goes with it.[46]

The largest Fiagro in terms of assets (USD 337 million), the Kinea Agro Fund, with 37,000 shareholders, has 37% of its assets in Agribusiness Receivables Certificates (CRAs) from sugar and ethanol plants. One of these CRAs was issued by Usina Itamarati, in the State of Mato Grosso, which leveraged USD 29.227 million by issuing “Green CRAs” despite the fact that its name was included on a blacklist for slave-like labour in 2008, in addition to several environmental violations.[47] The fund also invested in purchasing three CRAs from Usina Rio Amambai Agroenergia, in Mato Grosso do Sul, owned by the US company Amerra, which had 2,000 hectares embargoed by the Brazilian environmental agency in 2022 and is being investigated for dumping sugarcane waste in a lagoon. That did not stop the issuance and funding of USD12.6 million in "Green CRAs”.[48]

Fiagro XPAC11, managed by XP Investimentos and with 62,000 shareholders, has a "green" debenture (green bond) in its portfolio issued by Aço Verde Brasil (AVB), part of the Ferroeste group, which is said to have 100% sustainable charcoal from planted forests. The loss of diversity, water depletion, land grabbing and expulsions of local communities worldwide, created by the expansion of industrial forest monocultures, does not strip the investment of its "green" quality. In addition, XPAC11 has investments in the world's largest meat producers, such as Minerva, Mafrig and BRF, which are largely responsible for increased deforestation, public land grabbing, in addition to being the largest sector in Brazil responsible for subjecting workers to slave-like conditions.[49]

Bursting the financial bubble: reclaiming the commons to prevent future generations of dispossessed people

It is clear that Agro is not pop but debt – referring to the historic economic, social, and the environmental debts of Brazil.

Even if we consider the figure of the inflated 25% of GDP produced by agribusiness to be true, people cannot eat GDP! Export balances - and exports of soybean - are irrelevant when analysing social development, i.e., reduction of poverty, inequalities, hunger, and environmental damage. Although GDP is a useful indicator, the GDP of agribusiness includes, for example, the earnings of transnational corporations from seeds, agrochemicals, fertilisers, and machinery, as well as financial services. To a large extent, these corporate earnings are remitted to the countries where they are headquartered, and therefore do not remain in the country.[50]

Furthermore, this figure does not include the sector's enormous debt, in the order of trillions of Brazilian reals, nor does it take into account the amount foregone through tax exemptions.[51] [52] Soybean alone, for example, which accounts for half the value of agribusiness production in the country, is attributed almost USD 12 billion a year in tax breaks, twice the cost of removing the tax on the basic food basket.[53]If we include the costs of irreversible damage to the environment in the balance, such as contaminated territories and the spread of disease, along with pollution and genetic and soil erosion caused by the agribusiness industrial chain, the debt is unpayable.

However, it is important to realise that this is not just about Fiagros or the financialisation of agribusiness, land, and food systems. This alliance between financial capital, real estate - both urban and rural - and insurance companies means that an increasingly restricted and violent category of investors are transforming rights into private property and merchandise, playing a decisive role in determining the price of housing, land, food, transport, social security, energy, water, and sewage.

Preventing the privatisation of hitherto common goods and their subsequent financial valuation, recovering the meaning of so-called public goods and the common areas of community economies, in cities and in the countryside, which should be geared towards creating a dignified life for people, can provide some good pointers for avoiding a future generation of dispossessed people. Preventing a situation whereby the majority will be dispensed a meagre income, provided they finance the people responsible for expropriating them.

Land Fiagro: land and water grabbing and deforestation

Fund/Administrator | Description |

Fiagro GRWA11 (Greenwich Agro) Banco Daycoval S.A (management fee of 1.15% of net assets and 10% profit sharing) | 2,590 individual shareholders, 2 non-financial legal entities, 2 investment funds. Net worth: BRL 24.8 million (USD 5 million), 55% in fixed assets 40% in CRAs. The share price has risen 15% since its launch until November 2023. Share price BRL10 reais ((USD 2). *The Fund does not provide information about the BRL13 million (USD 2.6 million) invested in fixed assets. |

Fiagro FZDB11 XP Investimentos S.A (administration and management fee of 0.80% on initial net assets adjusted for inflation and 15% profit sharing) | 75 investors with investments over BRL1 million (USD 200,000). As of January 2024, the fund was restricted to investors with investments of more than BRL10 million (USD 2 million). Net worth: BRL 357.7 million (USD 72 million) on 13,500 ha of Farm Tabuleiro I, Correntina/Bahia. Lease of 9,300 hectares for soybean, maize and a little cotton until the 2035/2036 harvest to SLC Agrícola. Values in sacks of soybean/ha, on average BRL 120 (USD 24) a sack. For a non-irrigated area: BRL 13 per sack of soybean/ha; Irrigated area BRL 22.75 per sack of soybean/ha and irrigation expansion area BRL 14 per sack of soybean/ha. The share price rose 10% from its launch up to November 2023. Share price BRL100.00 reais (USD 20). |

XP investimentos S.A (administration and management fee of 0.80% on initial net equity adjusted for inflation and 15% profit sharing) | 477 qualified shareholders with investments of over BRL1 million (USD 200,000). As of January 2024, restricted to investors with investments of over BRL10 million (USD 2 million). Net equity of BRL345.4 million (USD 69.4 million) with 9,000 ha of 6 Xingu Farms in Balsas /Maranhão Lease of 5,500 hectares for soybean and a little maize to SLC Agrícola. Values in sacks negotiated at BRL159 (USD 32) per sack. 5 sacks of soybean/hectare until 2023/2024 and 13 sacks of soybean/ha until 2035/2036. Share price rose 22% from launch until January 2024. Share price BRL 96.00 (USD 19). |

Source: Funds' financial reports and monthly B3 Fiagros bulletins.

Illustration: Matheus Ribs

Infographic designer: Kartine Ribeiro Gomes

Infographic designer: Kartine Ribeiro Gomes

___________________________________

[1] Conversion 1 USD = BRL 4.97, using the Oanda currency converter on 11 March 2024.

[2] Humpec, “Formas de invertir em proyectos de agricultura en Mexico”.https://blog.humpec.com/formas-invertir-proyectos-agricultura and https://landing.humpec.com/invierte-en-oro-verde-mexicano#form

[3] GRAIN, “The avocados of wrath”, 4 May 2023. https://grain.org/en/article/6985-the-avocados-of-wrath

[4] Gastón Caligaris, “Acumulación de capital y sujetos sociales en la producción agraria pampeana (1996-2013)”, chapter entitled El caso de los “grandes pooles de siembra”, Buenos Aires: UbaSociales, 2017. https://www.teseopress.com/produccionagraria/

[5]Law 24.083/1992 and Law 24.441/94 regulate common investment funds and trusts, making sowing pools viable as a special niche for financial capital. Frederico and C. Gras. “Globalização financeira e land grabbing: constituição e translatinização das megraempresas argentinas”. In: Bernardes et al. (coord), 2017, p. 11-32.

[6] National Agrarian Census, 2018. Available at: https://cna2018.indec.gob.ar/informe-de-resultados.html

[7] Pedro Pereti, “Todo el poder a los pools”, 12 December 2023. https://www.pagina12.com.ar/694385-todo-el-poder-a-los-pools

[8] Madeleine Fairbairn, “Fields of Gold: financing the global land rush”, Ithaca [New York]: Maizeell University Press, 2020, p. 30-32.

[9] NCREIF Farmland Index. https://user.ncreif.org/data-products/farmland/. The cumulative return on agricultural land between 1983 and 2010 was above 15% in some markets, see below: Andrew Gunnoe, “The Political Economy of Institutional Landownership: Neorentier Society and the Financialization of Land”, Rural Sociology, 79 (4); 2014. P. 478–504, 2014: p. 492 and 493.

[10] NCREF Timberland Property Index. https://user.ncreif.org/data-products/timberland/. These lands reached cumulative rates of return of 26.75% per year. See Andrew Gunnoe. Ibid.

[11] USDA, Economic Research Service, February 2024. https://www.ers.usda.gov/data-products/chart-gallery/gallery/chart-detail/?chartId=58268

[12]Law 14.130/2021 amends Law 8.668 on Investment Funds to create Fiagros. See: Larissa Vitória, “Primeiro Fiagro do Brasil e outros credores de CRA decretam vencimento do título após calote parcial e podem executar garantias”, Seu dinheiro, 7 March 2024. https://www.seudinheiro.com/2024/bolsa-dolar/primeiro-fiagro-do-brasil-e-outros-credores-de-cra-decretam-vencimento-do-titulo-apos-calote-parcial-lvit/

[13]Military governments in the 1980s and then during the currency crisis in the 1990s securitised the debts of agribusiness and financial agents by replacing unpayable private bonds with treasury bonds, which made the Brazilian state the guarantor of agribusiness debts. Guilherme Delgado, “Do Capital Financeiro na Agricultura à Economia do Agronegócio”, Porto Alegre, UFRGS editora, 2012, p.86-87.

[14] Clarice Couto and others. “Falências no agronegócio ameaçam mercado de Fiagros que já soma R$ 34 bi” https://www.bloomberglinea.com.br/agro/falencias-no-agronegocio-ameacam-mercado-de-fiagros-que-ja-soma-r-34-bi/?utm_source=piano&utm_medium=email&utm_campaign=28909&source=piano-newsletter-br&pnespid=5r9sDX5AN7wFgqjdrSmrFZCBvwuxW5AmLLHlzOV2rR5mPBkQLWKs785Qg4Z7sTVBPgrgW_i4dA

[15]The Agribusiness Receivables Certificate (CRA) is a credit security that represents a promise to pay in cash or in production or rural property, issued exclusively by securitisation companies. The stock of CRAs increased by 92% between January 2022 and January 2024, according to the Ministry of Agriculture Bulletin.

[16] Luiz Henrique, “Usina Ester fa acordo com detentores de CRAs”, The AgriBiz, 6 June 2023 https://www.theagribiz.com/agribuzz/usina-ester-faz-acordo-com-detentores-de-cras/ and XPCA11 report, January 2024. https://fnet.bmfbovespa.com.br/fnet/publico/visualizarDocumento?id=609370&flnk

[17] This account is different from a CPF number (Brazilian individual taxpayer registry number). The same investor can have more than one account, resulting in a concentration of investments.

[18] Boletim Fiagro B3 of January 2024. https://www.b3.com.br/data/files/55/51/39/F1/DC98D8103152D4C8AC094EA8/Boletim%20Fiagro%20-%2001M24.pdf

[19] Individual investors do not pay tax on share returns provided that the Fiagros have more than 100 shareholders and hold up to10% of the shares issued or of the income distributed by the fund. As of 2024, to be exempt from tax a shareholder cannot accumulate over 30% of shares in the fund, with other relatives, or 30% of the income earned.

[20] Dividends are part of the profits distributed to fund shareholders or company partners, which can be paid annually or even monthly, depending on the regulations. The dividend yield is the annual dividend divided by the current value of the share, which gives the rate of return on the investment for the month.

[21] Katherine Rivas, “5 Fiagros para quem busca dividendos acima de 10% em 2024”. Estadão, 30 November 2023. https://einvestidor.estadao.com.br/investimentos/fiagros-para-dividendos-2024-investimentos/#:~:text=Segundo%20um%20levantamento%20da%20%C3%93rama,no%20CDI%20no%20mesmo%20per%C3%ADodo.

[22]From August 2022 until August 2023, the Selic rate, the benchmark for interest rates in the country, was at 13.75% per year.

[23] Anbima, “Raio X do investidor Brasileiro 6º edição”, 2023. https://www.anbima.com.br/pt_br/especial/raio-x-do-investidor-2023.htm

[24] Bruna Bronoski, “Boom de pessoas físicas no mercado financeiro vira alvo de capitalização do agronegócio”, O Joio e o Trigo, 3 March 2023. https://ojoioeotrigo.com.br/2023/07/boom-de-pessoas-fisicas-mercado-financeiro-agronegocio/

[25] Luiz Gerbelli, “Riqueza do agronegócio torna o Centro-Oeste a nova meca dos investimentos financeiros”. Estadão. 10 March 2023. https://www.estadao.com.br/economia/investidores-produto-financeiros-centro-oeste-agronegocio/#:~:text=Impulsionada%20pelo%20agroneg%C3%B3cio%2C%20a%20riqueza,em%20rela%C3%A7%C3%A3o%20%C3%A0%20popula%C3%A7%C3%A3o%20local.

[26] Carlos Walter Porto-Gonçalves. “Dos Cerrados e de suas riquezas: De saberes vernaculares e de conhecimento científico”, FASE, 2019: p.26-27. https://fase.org.br/wp-content/uploads/2019/12/PUBLICACAO_CERRADO-2.pdf

[27]Boletim CVM Agronegócio, September 2023.

[28] Nayara Figueiredo, “AGBI busca R$ 150 milhões para Fiagro “verde” e áreas para comprar”, Valor Econômico, 23 June 2023. https://valor.globo.com/agronegocios/noticia/2023/06/23/agbi-busca-r-150-milhoes-para-fiagro-verde-e-areas-para-comprar.ghtml

[29] GRAIN, “From land grab to soil grab - the new business of carbon farming”, 24 February 2022. https://grain.org/e/6804

[30] “Uber utilizo créditos de carbono generados en una granja que empleaba mano de obra esclava”, Timis, 19 February 2024. https://timis.es/uber-utilizo-creditos-de-carbono-generados-en-granja-mano-de-obra-esclava/and Carolina Bataier, “Projeto Jari de créditos de carbono engana comunidades e invade terras públicas no Pará”, De Olho nos Ruralistas, 19 February 2024.

[31]Thimothy Killeen, “What is most convenient in land distribution? | BOOK”, Mongabay, 5 March 2024.

[32] Report by AGBI Real Assets Agronegócio. https://agbi.com.br/agronegocio/

[33] Márcia De Chiara. “Supersafra derruba valorização de terra agrícolas em 2023, depois de ciclo de alta. Estadão” 6 February 2024.https://www.farmlandgrab.org/post/view/31999-brasil-supersafra-derruba-valorizacao-das-terras-agricolas-em-2023-depois-de-um-ciclo-de-alta

[34]Top 10 Variation in the closing price since the launch date of the B3 Monthly Bulletin of Investment Funds in Agro-Industrial Production Chains (FIAGRO) for November 2023 and January 2024.

[35] Matopiba is an acronym for the states of Maranhão, Tocantins, Piauí and Bahia, a region defined as one of the world's last agricultural frontiers, which has already caused the deforestation of 50% of the biome. Between August 2022 and July 2023, 11,000 km² of forests were cleared, the highest rate in the last eight years, 75% in the Matopiba region. Bahia saw the highest increase of deforestation, up 38%. Prodes Cerrado data: https://www.gov.br/ibama/pt-br/assuntos/noticias/2023/mma-divulga-prodes-cerrado-e-plano-para-o-bioma#:~:text=No%20per%C3%ADodo%20Prodes%20(agosto%20de,de%2026%25%20e%2027%25

[36] GRAIN, “Agribusiness and big finance’s dirty alliance is anything but “green””, 15 September 2021. https://grain.org/en/article/6720-agribusiness-and-big-finance-s-dirty-alliance-is-anything-but-green

[37] In 2017, a crowd of 12,000 people - of a total population of 12,600 (2010 Census) - took to the streets of Correntina with the slogan "No one will die of thirst on the banks of the Rio Arrojado" to protest the excessive abstraction of water by large farms. Lu Sodré, “Águas cercadas: como o agronegócio e a mineração secam rios no Brasil”. Brasil de Fato, 30 July 2020. https://www.brasildefato.com.br/2020/07/30/aguas-cercadas-como-o-agronegocio-e-a-mineracao-secam-rios-no-brasil

[38] Márcia De Chiara. “Supersafra derruba valorização de terra agrícolas em 2023, depois de ciclo de alta”, Estadão: 6 February 2024.https://www.farmlandgrab.org/post/view/31999-brasil-supersafra-derruba-valorizacao-das-terras-agricolas-em-2023-depois-de-um-ciclo-de-alta

[39] Leandro Gottems, “Ministério da Agricultura dá sinal verde a Fiagros”. Agrolink, 1 March 2024. https://www.agrolink.com.br/noticias/ministerio-da-agricultura-da--sinal-verde--a-fiagros_488754.html

[40]Amendment of Law 13.986/2020 regarding agro securities in Law 5.709/71, which imposes limits on the acquisition of land by foreigners.

[41] The term "grilagem" arose from a practice of falsifying land documents by placing the papers inside a closed box with crickets, which corroded and yellowed the papers, giving them the appearance of ageing. It is land grabbing or illegal occupation of stolen public and collective lands.

[42] GRAIN, CPT, AATR, ABRA. “From political coup to land destruction in Brazil”, 16 December 2020.

[43] GRAIN, “Regenerative agriculture was a good idea, until corporations got hold of it”. 1 December 2023. https://grain.org/e/7067

[44] Law 13.986/2020, subsequently amended by Law 14.421/22.

[45]The Cédula do Produto Rural (CPR), the first agribusiness security created in 1994 (Law 8929), is a security that represents rural production payable in product or financial settlement on its maturity date. The Law was amended both to expand the list of those who can issue the securities (to include not only rural producers but also input firms, marketing companies, processing companies) and to expand the concept of "rural products", with the regulation of the green CPR by Decree 10.828/2021. The CPR reached BRL 309 billion, an increase of 144% between January 2022 and January 2024. Boletim Finanças Privadas do Agro, February 2024. https://www.gov.br/agricultura/pt-br/assuntos/politica-agricola/boletim-de-financas-privadas-do-agro/boletim-de-financas-privadas-do-agro-fev-2024.pdf/view

[46] GRAIN, “An agribusiness greenwashing glossary”, 7 September 2022. https://grain.org/e/6877

[47] João Peres, “Fundos do agro impulsionam empresas com histórico de destamatamento, escravidão e grilagem”, O Joio e o Trigo, 20 July 2023.https://ojoioeotrigo.com.br/2023/07/fundo-do-agro-impulsiona-desmatamento

[48]Camila Ramos, “Usina Rio Amambaí capta R$ 60 milhões com “CRA verde”, Valor Economico, 15 March 2021. https://valor.globo.com/um-so-planeta/noticia/2021/03/15/usina-rio-amambai-capta-r-60-milhoes-com-cra-verde.ghtml

[49]Industrial livestock farming has been responsible for 46% of the 63,000 workers rescued from slave-like conditions since 1995. Environmental Justice Fundation, “Trabalho escravo no setor pecuarista: o caso de Mato Grosso e Mato Grosso do Sul”, November 2023. https://ejfoundation.org/resources/downloads/Trabalho-escravo-no-setor-pecuarista-o-caso-de-Mato-Grosso-e-Mato-Grosso-do-Sul.pdf

[50] The Agribusiness GDP data is produced by the Centre for Advanced Studies in Applied Economics (Cepea/Esalq), of the University of São Paulo (USP), financed by the Confederation of Agriculture and Livestock of Brazil (CNA) - the sector's largest trade body. The methodology used can be seen here:https://www.cepea.esalq.usp.br/br/pib-do-agronegocio-brasileiro.aspx

[51] In 2016, the sector's debt totalled BRL1.2 trillion (around USD 310.8 billion), according to the Attorney General's Office (PGFN). Oxfam, Brazil. “Terrenos da desigualdade: Terra, agricultura e desigualdades no Brasil rural”, São Paulo, November 2016. p. 18 and 19. https://www.cepea.esalq.usp.br/br/pib-do-agronegocio-brasileiro.aspx

[52] The so-called Kandir Law (Complementary Law 87/1996) prohibits tax on the distribution of agricultural and mining production for export. Agribusiness paid less than BRL16,000 reais (USD 3,200) in export tax in 2019. With agrochemicals alone, around BRL 6.8 billion (USD 1.3 billion) no longer entered public coffers between 2011 and 2016. Maurício Angelo, “Uma sugestão para Paulo Guedes: acabar com a mamata das isenções fiscais bilionárias para agrotóxicos”. The Intercept, 7 January 2019. https://oxfam.org.br/wp-content/uploads/2019/08/relatorio-terrenos_desigualdade-brasil.pdf

[53] Arnoldo de Campos. “O custo da soja para o Brasil”, 2023.https://www.idsbrasil.org/wp-content/uploads/2023/10/O-custo-da-soja-para-o-Brasil_renuncias-fiscais-subsidios-e-isencoes-da-cadeia-produtiva.pdf