In November 2022, word got out that Ferdinand Marcos Jr, the freshly minted president of the Philippines, wanted to set up a sovereign wealth fund. People scratched their heads. What wealth? The Philippines is mired in debt! It was quickly understood that this was a kind of vanity project, meant to improve the image of a man who came to power because of his family name. Marcos’ father ruled the Philippines from the mid-1960s to the mid-1980s with an iron fist. Known more for kleptocracy and the brutality of martial law, the Marcos name needed a face-lift, local media put it. Marcos boasted that a sovereign wealth fund would boost investor confidence and attract resources to fund big projects in infrastructure or agriculture. He even dubbed it “Maharlika Fund”, a nod to the mythical warrior figure that his father claimed to personify during World War II.

Vanity aside, Marcos’ proposal raised fears of graft and corruption. After all, not long ago, Malaysia’s sovereign wealth fund (known as 1MDB) was exposed as a multi-billion dollar money laundering scheme for the personal benefit of Prime Minister Najib Razak, who now sits in jail. Yet, Marcos managed to get his proposal onto his country’s legislative agenda in a matter of weeks, and brought it to international investors in Davos and Tokyo for their approval as well.

What are these “sovereign wealth funds”? How are they being used? What link, if any, do they have with people’s struggles around food sovereignty, land grabbing and today’s deepening climate crisis?

Rise of sovereign wealth funds

The first sovereign wealth funds were set up in the 19th century, and grew slowly throughout the 20th. The idea, at first, was rather simple. If a state has excess resources – perhaps mineral wealth or a sudden boom in foreign exchange from exports – these should be tucked away for future use for the benefit of society.

Norway is the classic example. In the late 1960s, oil was discovered off its coast. Overnight, the country become unfathomably rich. After much debate, the government decided to set up a wealth fund – basically a piggy-bank belonging to all Norwegians. It is fed by a tax levied on the oil and gas extracted from Norway’s seabed, plus the revenues of Norway’s state-owned oil and gas companies. This wealth is meant to be used “for present and future generations”. To ensure this, no one is allowed to touch the underlying pot of money itself, but the interest it earns each year goes into the national budget to pay for things like public health care, generous parental leaves, retirement pensions and public infrastructure. In concrete terms, Norway’s wealth fund contains $1.1 trillion. That money is invested in 9,000 publicly-listed companies across 70 countries around the world. The investments generate a return of about 3% a year, which is what goes into the national budget to provide everyone in Norway with those public services. It has become a source of national pride and unity across the political spectrum.

Many sovereign wealth funds were set up with a similar logic. The “wealth” may come from diamonds (Botswana) or copper (Chile), foreign currency reserves (China) or export earnings (Saudi Arabia). Even the state of Texas in the United States wrote into its constitution back in the 1850s that “available public lands” should be used to finance public schools. To do this, lands were either sold outright or were leased with the proceeds feeding a Permanent School Fund (a sovereign wealth fund) run by a trio of local civil servants. In all of these cases, the funds are created with resources that arguably belong to everyone and serve a public interest objective such as guaranteeing social rights (e.g. retirement for all in Norway) or covering national budget deficits in times of crisis (e.g. as happened with Covid-19 in Peru) or providing children with access to education (Texas).

Recently, however, governments have started diverging from this logic. Increasingly, sovereign wealth funds are being set up with no resources or wealth or sovereign character to speak of. Indonesia’s sovereign wealth fund, which was set up in 2021, is more like a “development” fund. It aims to secure foreign investment from companies, banks and funds in order to build local infrastructure and energy projects. Not much different from what the government already does. The Philippines’ proposal is more like a “public-private partnership” fund, as foreign investors will be asked to do joint ventures with the state or with local businesses. At one point, the government was proposing that the fund should be handed over to the private sector and listed on the stock market! Quite a number of small countries with no surpluses to speak of have set up sovereign wealth funds by offering citizenship to wealthy individuals (leading to corruption scandals as well).

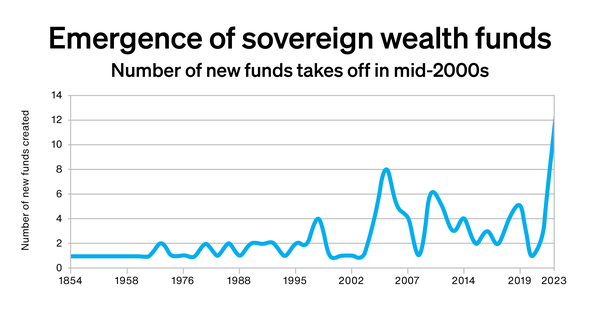

Over the past two decades, the number of sovereign wealth funds has surged (see graph) and there are now more than 100 sovereign wealth funds around the world.[1] Collectively, they hold $10 trillion – which makes them the third largest economy, after the US and China, if they were a country. That figure is expected to reach $17 trillion by 2030. While most sovereign funds are national in scope, some are sub-national. The state of Queensland, in Australia, has one. Palestine has one. Even the city of Milan has one.

Some of these funds invest only abroad, some invest only at home and some do both. Key sectors they put their money in, to capture earnings, include energy, technology, health, finance and real estate. All told, sovereign funds are so massive that most people have probably had some connection to them, as they own bits of Alibaba, Flipkart, Uber, Slack, Grab, major airports, the world’s top football teams and social media like Twitter. Anyone paying for these is actually helping sovereign wealth funds take money home.

And while it seems to be a trend among political elites these days to think that setting up such structures can bring funds into the global South, 80% of sovereign wealth fund assets is currently parked in Europe and North America. In fact, one-third is in the US alone.

Agriculture: a critical concern

In dollar terms, food and agriculture represent just 2-3% of all sovereign wealth fund investments. While that sounds small, it is a politically sensitive and strategic sector for many governments. Contributing to national food security has been a historic role for sovereign funds, and it is a vital one for those of Singapore and the Gulf states.

At least 42 sovereign funds are currently invested in food and agriculture (see table). Some are major players, but many are less visible (see box). Their investments may be in largescale farmland acquisitions and production, such as orange groves in Brazil, cattle ranches in Australia or vertical pig farms in China. Some take the form of ownership stakes in global food commodity traders that ship grains, oilseeds and coffee across our oceans, like Bunge, COFCO or Louis Dreyfus. Yet others are positions in food retail systems like supermarket chains or delivery services, and the digital technologies that these operations increasingly rely on.

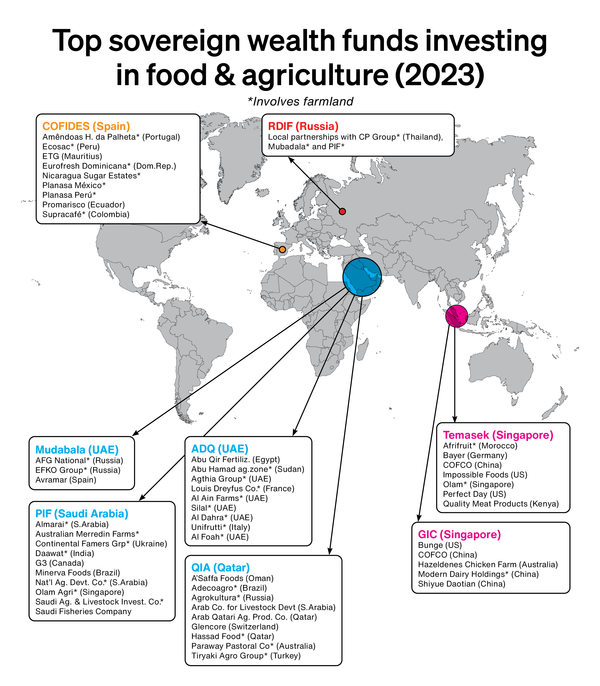

A handful of actors form the centre of gravity of global agricultural investing by sovereign funds. They are Temasek and GIC in Singapore; PIF in Saudi Arabia; Mubadala and ADQ in UAE; QIA in Qatar; RDIF in Russia; and COFIDES in Spain (see map). The Singaporeans and the Gulf states invest with their own food needs as a priority. RDIF brings big investors into Russia to help finance its export-oriented agribusiness sector. And COFIDES funds food projects around the world with one catch: a Spanish company must be directly involved in and profit from it, such as Borges with almond production in Europe or Pescanova with fish farming in Latin America. (Actually, there is a second catch: all of COFIDES’ overseas food and agriculture investments are loans.[2])

Quite a number of sovereign wealth fund ventures in agriculture are linked to concerns about land and water grabbing, whether directly and indirectly. In December 2022, Abu Dhabi’s government-owned ADQ, which has $110 billion in assets, got hold of 167,00 hectares of farmland in northeast Sudan.[3] It plans to grow sesame, wheat, cotton and alfalfa there, while it builds a massive new port nearby to ship the goods out. ADQ already owns:

- 45% of Louis Dreyfus Company, with its massive land holdings in Latin America, growing sugarcane, citrus, rice and coffee;

- a majority stake in Unifrutti, with 15,000 ha of fruit farms in Chile, Ecuador, Argentina, Philippines, Spain, Italy and South Africa; and

- Al Dahra, a large agribusiness conglomerate controlling and cultivating 118,315 ha of farmland in Romania, Spain, Serbia, Morocco, Egypt, Namibia and the US.

Therefore, the concerns are quite serious. Al Dahra stands accused of draining aquifers in Arizona, just so that it can produce hay to transport back to UAE to feed local dairy herds.[4]

Saudi Arabia’s Public Investment Fund (PIF), one of the world’s top ten sovereign wealth funds in terms of assets, has $13.7 billion invested in agriculture. It owns several massive agribusiness conglomerates focused on livestock, dairy and fisheries. In 2021, it took 100% control of the Saudi Agricultural and Livestock Company (SALIC) which is engaged in meat and cereal production in Canada, Ukraine, India, Brazil, Australia and the UK.[5] The scale is enormous. In India, PIF produces its staple, basmati rice. From Brazil, it gets its beef. In Australia, it operates 200,000 ha for sheep grazing and also buys lamb and mutton directly from producers. In Ukraine, it has 195,000 ha growing wheat, barley, maize and rice. PIF also owns 35% of Olam Agri, a major palm oil producer, and is building the largest vertical farm in the entire Middle East and North Africa region.[6] It is very strange, then, to learn that PIF’s new green financing instrument will explicitly exclude funding for any projects or expenditures associated with industrial agriculture or livestock![7] It shows the doublespeak of investors that expand intensive industrial food systems while needing to flash climate credentials.

Another very big player is Qatar. Its sovereign wealth fund has massive land holdings in Australia, through a stake in the 4.4 million ha Paraway Pastoral Company dedicated to livestock production. The fund allows Qatar to source its organic food supplies through Canada’s Sunrise Foods, which operates in Turkey, Netherlands, Russia, Ukraine and US. It owns poultry and seafood companies in Oman, and is now developing agriculture supply chains in East Africa. The Qatari wealth fund is connected to a Russian oil company which owns 50% of Agrokultura, which operates 200,000 ha of farmland in Russia. It also owns 14% of AdecoAgro with its 472,862 ha hectares under production in Argentina, Brazil and Uruguay. It is now going into Kazakhstan for the same purposes – and in direct competition with the UAE.[8]

It is important to note that many of these arrangements between sovereign wealth funds and global agribusiness involve political guarantees. Qatar is one of the biggest investors in Glencore, with whom it has a deal to ensure its access to grains and shipping services in case of need. The same is true with Qatar and Turkey’s Tiryaki Agro Group. The fund’s agricultural arm, Hassad Food, has its own agreement with Sunrise Foods which ensures that in the event of any shortage in the Qatari market, the country’s need for grain, oilseeds and wheat will be met on a priority basis.[9] Similarly, when Abu Dhabi’s ADQ bought 45% of Louis Dreyfus – the world’s third largest commodity trader – it signed a side deal giving it priority access to food shipments in times of global crisis, as the world experienced recently during both Covid-19 and the Russian invasion of Ukraine.[10]

It is fair to say that the political strategy of leveraging sovereign wealth to get access to global food supplies works. What is never mentioned is at what cost. For many of these big investment projects expand and entrench largescale corporate agribusiness, with its contingent slew of land conflicts, water pollution, indigenous rights abuses, labour violations and spiralling climate emissions. And when it comes to the Gulf states or Singapore, these are very small populations draining the resources of much bigger ones. With sovereign funds, scale is baked in. Even when they do try to reckon with social and environmental contingencies, as in the case of PIF, their attempts at making investments green or socially responsible are shallow at best. Only Norway’s stands out as making strong commitments to scrutinise and withdraw from agribusiness companies associated with social and ecological crimes, as it has done with meat packers and soy producers in Brazil (Minerva, Marfrig, SLC Agricola and JBS) as well as rubber giant Halcyon Agri.[11]

So, to answer the question: what do these funds have to do with food sovereignty? The answer is: it’s twisted. They do provide food security for a few countries. And political elites increasingly like to use the term food sovereignty to characterise these missions, as it serves their nationalist, territorial and militarist frameworks.[12] But sovereign wealth funds crush real visions of food sovereignty as they take resources away from local communities and push a capitalist, industrialist food system – be it green or not.

Putting the public interest first

Sovereign wealth funds can be a good idea if they really are sovereign (run by the people), if the resources they harness are democratically sourced and organised, and if they have a genuine public welfare mandate. We actually need more commitment to public approaches to reverse the growing inequality and privatisation that is undermining people’s rights to healthcare, housing, transportation, food, education and retirement in most countries around the world.

But there is a danger. There are increasing calls to set up sovereign wealth funds to solve government problems – from building a new capital city in Indonesia to plugging an alleged deficit in France’s pension system. But these newer funds are just tools to channel money into government coffers or private enterprises. They are not built on any collective resource or aimed at protecting a public wealth for the benefit of future generations. They seem to have little to do with traditional sovereign wealth funds, apart from the name. For that reason, they should be scrutinised and if they don’t genuinely serve the public interest they should be stopped. Similarly, those that contribute to land or water grabbing should be challenged and stopped, too.

Agriculture may not be the number one sector that these funds gravitate towards to generate wealth. But politically, geopolitically and strategically, food security is a core concern of theirs and will continue to be, requiring our critical scrutiny as well.

We need good public services that provide for public well-being. Sovereign wealth funds – despite their name – need to be put to a more scrupulous test to see if they have a role to play in that agenda.

Less visible players: Big players aside, many sovereign wealth funds participate in financing the direction of food and agriculture.[13]

• Angola’s sovereign wealth fund is investing in food and agriculture in Africa through a private equity fund that is targetting the production of maize, beans, soybeans, rice and cattle.

• Australia’s sovereign wealth fund has a Future Drought Fund since 2019. Currently holding A$4.5 billion, its sole aim is to "provide secure, continuous funding to support initiatives that enhance the drought resilience of Australian farms and communities." Its investments must deliver returns of 2-3% above the consumer price index.

• Bolivia has a sovereign wealth fund that was set up in 2012 with state surplus funds and a loan from the central bank. It invests domestically in both public and private enterprises involved in honey production, fruit processing, aquaculture, dairy, quinoa and stevia.

• Brunei’s new sovereign wealth fund is considering investing in agriculture, in partnership with the Malaysian Investment Development Authority.

• Not much is known about how China’s sovereign wealth funds invest. The China Investment Corporation has $1.3 trillion, making it the largest in the world. It invests in agriculture overseas and reported a remarkable return of 14.27% on its overseas holdings in 2021. Equally remarkable, alternative investments, which include private equity and farmland, are said to account for 47% of its overseas portfolio. China's National Social Security Fund is also a sovereign wealth fund and is invested domestically in agriculture through its private equity portfolio.

• France’s sovereign fund is known to be a big investor in agriculture and food, both domestically and abroad. One very controversial foreign project it was connected to was led by Arise IIP, a subsidiary of Olam until 2022, in Chad.[14]

• Gabon’s sovereign wealth fund, built from oil revenues, runs a private equity fund that invests in the food and agriculture sector. It also invests directly in agriculture and farmland projects at home.

• The National Development Fund of Iran has some $24 billion, most of it from oil and gas revenues and all of it invested domestically. According to some sources, 1% is invested in water and agriculture, including farmland ownership, a sector the fund wants to invest more in.

• Ithmar Capital, a state investment company, serves as Morocco’s sovereign wealth fund. Details are lacking but their strategy is to co-invest in Moroccan agribusiness operations with foreigners such as Spain’s COFIDES or Gulf state investors.

• Nigeria, like Abu Dabhi and Spain, has its sovereign wealth fund investing in fertiliser production. This is a very strategic concern.

• Palestine’s sovereign wealth fund is a public company that does local impact investing. Its initial funds came from the Palestinian Authority. It is invested in a 50 hectares seedless grape farm, looking into investing in animal feed production and helping set up a National Agriculture Investment Company.

• Türkiye Wealth Fund has 2% of its investments in food and agriculture, as of 2019.

• In the US, the states of Texas, New Mexico and Alaska have sovereign wealth funds that are heavily invested in farmland, whether directly or through private equity funds. The agribusiness operations they fund are in some cases domestic and in others overseas (usually in the Southern Cone of Latin America or Australia).

• Vietnam’s State Capital Investment Corporation is invested in agriculture/farmland through a joint venture with the State General Reserve Fund of Oman, showing how co-investing is a common strategy of sovereign funds.

Sovereign wealth funds invested in farmland/food/agriculture (2023) | |||

Country | Fund | Est. | AUM (US$bn) |

China | CIC | 2007 | 1351 |

Norway | NBIM | 1997 | 1145 |

UAE - Abu Dhabi | ADIA | 1967 | 993 |

Kuwait | KIA | 1953 | 769 |

Saudi Arabia | PIF | 1971 | 620 |

China | NSSF | 2000 | 474 |

Qatar | QIA | 2005 | 450 |

UAE - Dubai | ICD | 2006 | 300 |

Singapore | Temasek | 1974 | 298 |

UAE - Abu Dhabi | Mubadala | 2002 | 284 |

UAE - Abu Dhabi | ADQ | 2018 | 157 |

Australia | Future Fund | 2006 | 157 |

Iran | NDFI | 2011 | 139 |

UAE | EIA | 2007 | 91 |

USA - AK | Alaska PFC | 1976 | 73 |

Australia - QLD | QIC | 1991 | 67 |

USA - TX | UTIMCO | 1876 | 64 |

USA - TX | Texas PSF | 1854 | 56 |

Brunei | BIA | 1983 | 55 |

France | Bpifrance | 2008 | 50 |

UAE - Dubai | Dubai World | 2005 | 42 |

Oman | OIA | 2020 | 42 |

USA - NM | New Mexico SIC | 1958 | 37 |

Malaysia | Khazanah | 1993 | 31 |

Russia | RDIF | 2011 | 28 |

Turkey | TVF | 2017 | 22 |

Bahrain | Mumtalakat | 2006 | 19 |

Ireland | ISIF | 2014 | 16 |

Canada - SK | SK CIC | 1947 | 16 |

Italy | CDP Equity | 2011 | 13 |

China | CADF | 2007 | 10 |

Indonesia | INA | 2020 | 6 |

India | NIIF | 2015 | 4 |

Spain | COFIDES | 1988 | 4 |

Nigeria | NSIA | 2011 | 3 |

Angola | FSDEA | 2012 | 3 |

Egypt | TSFE | 2018 | 2 |

Vietnam | SCIC | 2006 | 2 |

Gabon | FGIS | 2012 | 2 |

Morocco | Ithmar Capital | 2011 | 2 |

Palestine | PIF | 2003 | 1 |

Bolivia | FINPRO | 2015 | 0,4 |

AUM (assets under management) figures from Global SWF, January 2023 | |||

Engagement in food/farmland/agriculture assessed by GRAIN | |||

[1] Important sources used for this report include: Javier Capapé (ed), “Sovereign wealth funds 2021”, IE University, Madrid, Oct 2022, https://docs.ie.edu/cgc/SWF%202021%20IE%20SWR%20CGC%20-%20ICEX-Invest%20in%20Spain.pdf; Global SWF, "2023 Annual report", New York, Jan 2023, https://globalswf.com/reports/2023annual; the websites of Global SWF (https://globalswf.com) and SWF Institute (https://www.swfinstitute.org/) as well as Preqin Ltd.

[2] See the COFIDES database, sector “Agri-food”, https://www.cofides.es/en/projects?field_direccion_country_code=All&field_sector_target_id=2

[3] Reuters, “Sudan to develop Red Sea port in $6-bln initial pact with Emirati group”, 13 Dec 2022, https://www.farmlandgrab.org/31347.

[4] Ella Nilsen, “Wells are running dry in drought-weary Southwest as foreign-owned farms guzzle water to feed cattle overseas“, CNN, 27 Nov 2022, https://edition.cnn.com/2022/11/05/us/arizona-water-foreign-owned-farms-climate/index.html

[5] See SALIC website: https://salic.com/

[6] AeroFarms, “PIF and AeroFarms sign joint venture agreement to build indoor vertical farms in Saudi Arabia and the wider MENA region”, 1 Feb 2023, https://www.aerofarms.com/2023/02/01/pif-and-aerofarms-sign-joint-venture-agreement-to-build-indoor-vertical-farms-in-saudi-arabia-and-the-wider-mena-region/

[7] Public Investment Fund, “Public Investment Fund Green Finance Framework”, February 2022, https://www.pif.gov.sa/Investors%20Files%20EN/PIF%20Green%20Finance%20Framework.pdf

[8] See Hassad Food, “Hassad signs MoU with Baiterek to discuss investment projects that supports food security”, 12 Oct 2022, https://www.hassad.com/2022/10/12/hassad-signs-mou-with-baiterek-to-discuss-investment-projects-that-supports-food-security/ and Global Sovereign Wealth Fund, “Gulf funds drawn into soft power battle over Kazakhstan”, 25 Aug 2021, https://globalswf.com/news/gulf-funds-drawn-into-soft-power-battle-over-kazakhstan

[9] See Hassad Food, “Strategic local and international investments along with global partnerships to satisfy the market needs from grains and wheat”, 28 Mar 2022, https://www.hassad.com/2022/03/28/strategic-local-and-international-investments-along-with-global-partnerships-to-satisfy-the-market-needs-from-grains-and-wheat/

[10] Reuters, “Commodity group Louis Dreyfus completes stake sale to ADQ”, 10 Sep 2021, https://www.reuters.com/world/middle-east/commodity-group-louis-dreyfus-completes-stake-sale-adq-2021-09-10/.

[11] See Fabiano Maisonnave, “Norway oil fund omits meatpacker JBS from deforestation watch list “, Climate Fund News, 4 Apr 2018, https://www.climatechangenews.com/2018/04/04/norway-oil-fund-omits-meatpacker-jbs-deforestation-watch-list/, Earthsight, “World’s largest pension fund dumps shares in beef firm in wake of corruption scandal”, 24 July 2018, https://www.earthsight.org.uk/news/idm/worlds-largest-pension-fund-dumps-shares-beef-firm-wake-corruption-scandal and Paulina Pielichata, “Norway sovereign wealth fund divests Halcyon over environmental concerns”, Pensions & Investments, 27 Mar 2019, https://www.pionline.com/article/20190327/ONLINE/190329915/norway-sovereign-wealth-fund-divests-halcyon-over-environmental-concerns

[12] “L’Afrique sur le chemin de l’autosuffisance alimentaire”, Seneplus, 27 Feb 2023, https://www.seneplus.com/developpement/lafrique-sur-le-chemin-de-lautosuffisance-alimentaire

[13] Main sources for this box are each fund’s respective website, news clippings and Preqin Ltd.

[14] Arise, "Bpifrance and Arise IIP establish a partnership to foster agricultural materials processing and co-industrialisation projects on a pan-African scale", 15 February 2023, https://www.ariseiip.com/bpifrance-and-arise-iip-establish-pan-african-partnership/ , and Benjamin König, "Arise IIP, la firme qui dépouille les paysans africains", L'Humanité, 4 April 2023, https://www.humanite.fr/monde/tchad/arise-iip-la-firme-qui-depouille-les-paysans-africains-789407