Cheap meat for China’s growing urban population was supposed to be the payoff. But in 2008, prices for pork spiked because of a massive disease outbreak that swept through China’s pork industry, and now the country is on the verge of a more serious round of food inflation as a drought in the US causes global prices for soybeans to surge. On top of this, China’s consumers have had to contend with numerous food safety scandals and environmental disasters brought about by the shift to industrial meat production.

")

Power plays for China’s maize supply

The next frontier

A simple solution

The world does not need to go down this path. In the face of yet another spike in prices for global agricultural commodities, China can put the brakes on industrial meat production, start supporting small scale livestock farming based on local feed resources, and ends its aggressive efforts to convert farmers into cheap labourers.

|

Box 1: From farms to factories

Ten years ago in China’s main pork producing provinces Fujian, Guizhou, Hainan, Hunan or Jiangsu, you would be hard pressed to find a household that didn’t keep half a dozen pigs. Today such homes are rare.

Despite government subsidies and rising meat prices, the number of Chinese households raising pigs dropped by half in 2008 alone, and has continued to decline ever since. People in China’s cities may be eating more pork, but villagers are eating – and earning – less.[7]

China’s 200 million farming households have average incomes less than a third of their urban counterparts and it is hard to find evidence of China’s booming meat consumption in the average Chinese village.

Yet pigs have long been central to life in much of rural China. They have enabled families to convert kitchen waste and farm residue into meat for sale or household consumption and into manure for their fields. But low prices and policies favouring large farms and urban migration have forced many Chinese households to give up their pigs. Now factory pig farms dot the countryside, spewing enormous quantities of waste that they cannot safely dispose of.

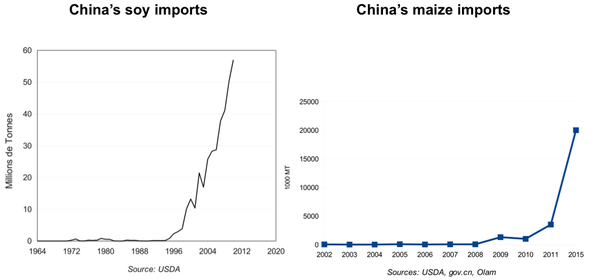

One of the consequences of this shift to factory farms, not only for pigs but also for poultry and other livestock, has been a massive growth in demand for industrial animal feed. The average pig raised in a Chinese factory farm eats around 350 kg of grain to grow to slaughter, while a pig raised on a Chinese family farm eats only 150 kg because it also consumes household waste and other non-grain, local feed sources. China is not only eating more meat these days, its farm animals are eating more crops – much more than what is produced in China.[8]

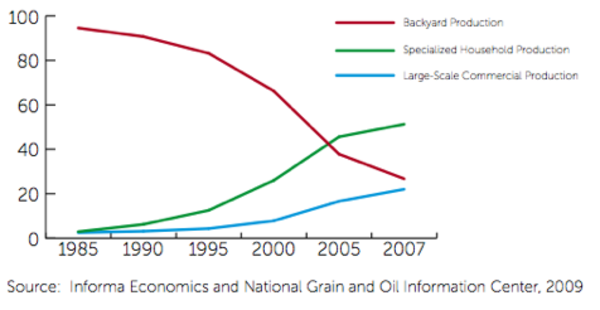

Figure 1. Share of total pig production in China by farm type, 1985-2007 (%).

|

|

Box 2: Ripple effects

Ituzaingó is just one of the communities affected by the massive expansion in soybean production in the Southern Cone of Latin America that followed from the opening of China’s soybean market to imports in the late 1990s.

"We used to have farms, and cows and fruit trees," says Sofía Gatica, a resident of the community of Ituzaingó, Argentina. "But they destroyed all that and planted genetically modified soybeans."[9]

Ituzaingó is just one of the communities affected by the massive expansion in soybean production in the Southern Cone of Latin America that followed from the opening of China’s soybean market to imports in the late 1990s.

Like other communities in the path of the soy boom, Ituzaingó lost more than just local food production. Every year in Argentina over 50 million gallons of pesticides are aerially sprayed on soybeans. Because of the aerial spraying of pesticides on the surrounding soybean fields, its cancer rate is now 40 times Argentina’s national average. Sofía Gatica's daughter died when she wa[c]s three days old from kidney failure caused by exposure to pesticides.

|

|

Box 3: Some Chinese companies with overseas agriculture projects

Chongqing Grain Group (CGG)

State-owned CGG has set aside US$3.4 billion for an overseas expansion that includes a 200,000 ha soybean farm in Brazil, a 130,000 ha soybean farm in Argentina's Chaco province, and plans to produce oilseed rape in Canada and Australia, rice in Cambodia and palm oil in Malaysia.

Beidahuang

State-owned Beidahuang manages over 2 million ha of farmland in the province of Heilongjiang. In Argentina, it is pursuing a partnership with Cresud, the country’s largest farming company, to acquire farmland. A US$1.4-million deal it signed with the governor of Río Negro province to secure a supply of soybeans, maize and other crops for 20 years from farms covering 320,000 ha was suspended by court order. Beidahuang is awaiting approval for a project to develop 200,000 ha of rice, maize, and other crops in the Philippines and is reported to have made offers on a number of farms in Western Australia, amounting to about 80,000 ha of land. Heilongjiang Province, meanwhile, has leased 426,667 ha of land in Russia.

Sanhe Hopeful

Privately owned Sanhe Hopeful says it will invest US$7.5 billion in the Brazilian state of Goias to secure six million tons of soybeans per year. It also has a joint venture with Argentine businessman Francisco Macri to produce and ship soybeans from Argentina's Northwest through the port of Santa Fé.

ZTE Corp

ZTE, China's largest telecommunications company, acquired 30,000 ha of oil palm plantations on Indonesia's Kalimantan Island, 50,000 ha for cassava production in Laos, and a 10,000 ha farm in Sudan for maize and wheat. In the Democratic Republic of the Congo it has two pilot farms and a 100,000 ha concession for an oil palm plantation that it has yet to develop.

Pengxin Group

Shanghai real-estate company Penxin Group invested more than US$20 million in a 12,500 ha Bolivian soybean and maize farm, established large-scale farms in Cambodia and Argentina, is negotiating to buy 200,000 ha of land in Brazil for soybeans and cotton, and purchased 16 dairy farms in New Zealand.

Tianjin State Farms Agribusiness Group Company

Tianjin State Farms acquired 2,000 ha of land in Bulgaria to grow maize, alfalfa and sunflower for export to China and is pursuing negotiations for a further 10,000 ha.

Shaanxi State Farm

Shaanxi State Farm signed a US$120-million investment agreement with the government of Cameroon that includes a long-term lease on 10,000 ha of land where the company intends to produce rice, maize, and cassava.

|

|

Box 4: Major impacts of the industrialisation of meat production in China

Industrialisation of livestock production, combined with liberalisation of the soybean sector, have resulted in a number of serious consequences for the environment, public health, and smallholder farmers. The following is a summary of five major impacts, all of which challenge the notion that industrial agriculture can solve food security needs now or in the future.

Environmental impacts

1. The massive increase of animal waste from industrial livestock operations is the main source of water pollution in China today. China's first pollution census – conducted in 2012 – found that the combined impacts of livestock farming and fertiliser and pesticide runoff from fields, surpassed industry as the county’s biggest source of water pollution. Rural people who depend on polluted waterways for household and agricultural use are worst affected in the short-term, but the dead zone that has developed in the East China Sea from excess nitrogen and phosphorus – directly related to industrial meat production – is a sign of larger-scale ecological crises in the longer term.

2. Industrial meat production also contributes significantly to increased greenhouse gas emissions, to the steep decline in indigenous livestock breeds and native soybean varieties, and to the emergence of antibiotic-resistant bacteria that threaten human and animal health.

Health and dietary impacts

1. Food safety has become a hot button issue in China along with the industrialisation of agriculture in general and livestock production in particular. From the highly publicised melamine milk scandals and animal feed and meat recalls, to the heavy metal, pesticide, and mycotoxin residues commonly found in meat, food safety issues are endemic to today’s industrial meat industry.

2. China's urban middle- and upper-classes are eating more meat, more often while spe[d]nding a declining share of household income on food . Rural residents, on the other hand, eat only half as much meat as their urban counterparts, but spend a larger share of their income on food (43.7% of rural income, versus 37.9% of urban income). In a sign of this growing inequality, urban Chinese are suffering increasingly from diet-related diseases of affluence (coronary heart disease, type 2 diabetes, obesity, and a range of cancers), while meat remains a luxury to many in rural China, where 150 million people fall below the US$1.25 per day poverty guideline, with another 140-230 million (20-30% of the rural population) precariously close to joining them in cases of illness, natural disasters, or economic recession.

Smallholder and rural livelihood implications

1. Smallholder farmers living in China’s vast rural regions are most vulnerable as a group to the livelihood transformations that result from the industrialisation of meat production. In the new agribusiness-led meat economy, smallholder livestock farmers struggle for market access against severe disadvantages in terms of evolving meat quality standards that favour leaner pork, safety requirements based on international standards, and the structure of state subsidy programs that provide support to the agriculture industry. Concurrently, small-scale soybean farmers are faced with cheap GM imports, a struggling domestic soybean crushing industry, and infrastructural challenges of getting their harvest to potential markets. These farmer households are continually losing money, and many have already had to give up livestock and/or soybean production.

(This box was written by Mindi Schneider and is based on her study “Feeding China’s Pigs: Implications for the Environment, China’s Smallholder Farmers and Food Security,” IATP, May 2011)

|